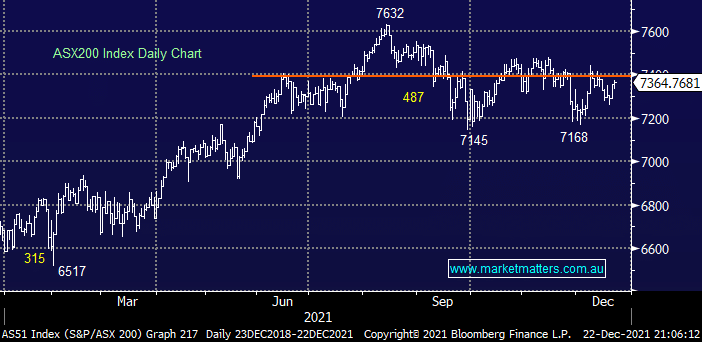

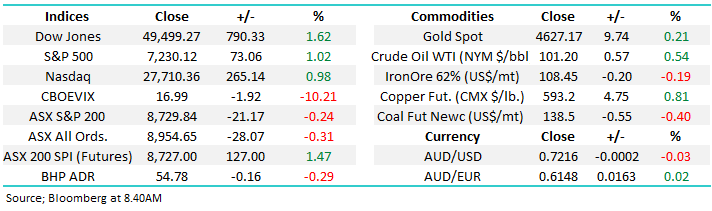

The ASX200 closed higher yesterday in subdued trading and with only 2-days remaining until Christmas Day it’s hard to imagine anything new after stocks have traded sideways for 6-months – we may have received a plethora of economic and humanitarian news since May but equities simply haven’t moved. Wednesday only saw 56% of the ASX200 rally but with a 2.6% advance by the Tech Sector it was enough to offset an intra-day reversal in the iron ore names as the bulk commodity backed off from fresh 10-week highs.

While risk assets were quiet, National Australia Bank (NAB) stealthily raised its fixed rate mortgages for the 2nd time this month making it a 0.6% hike since the 2nd of December. Omicron might be dominating the press / media but financial markets appear far more focused on inflation and potential rate hikes by central banks through 2022. Banks are facing challenges with their long-term funding costs and these increases will ultimately be passed along to the consumer so banks can alleviate margin pressure. Conversely shorter dated bond yields have continued to drift lower after surging higher through October, MM believes further inflation concerns are likely in Q1 of 2022 which is should push yields and value stocks higher i.e. Resources & Banks.

The local market is up over 100-points so far in December and a Santa Rally into 2022 remains a definite possibility as liquidity slowly but surely dries up into the holiday season – but it hasn’t felt like the style of move I’ve witnessed almost like clockwork in previous years, perhaps it’s simply too much to ask after the rally enjoyed by stocks since March 2020. Our stance hasn’t changed over recent weeks / months although it’s a little disappointing that the ASX200 has struggled to emulate US stocks through the 2nd half of the year:

- The trends up and while MM believes its maturing like a fine red we see no reason to sell anything except strength until further notice.

- In similar vain if we were traders we couldn’t be short today considering the seasonal statistics which could still kick in at any stage.

US equities enjoyed a strong session overnight as home sales and consumer confidence trumped Omicron fears as investors continue to believe it’s only going to have a temporary impact on economic activity due to its mild symptoms. The Dow rallied over 250-points and the SPI Futures are pointing to an open up around 40-points with gains likely to be broad based if we follow the lead from the US.

MM remains mildly bullish the ASX targeting fresh highs into 2022

Add To Hit List