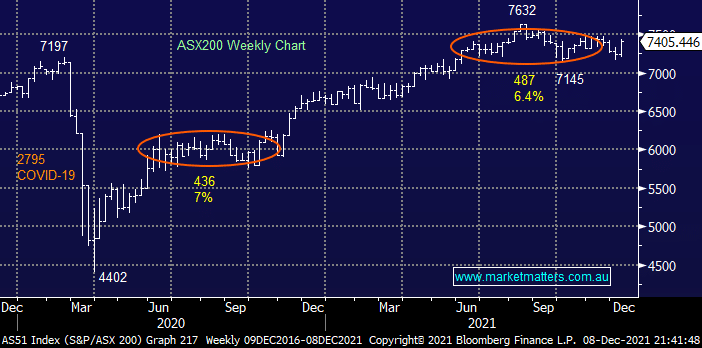

The ASX200 roared higher on Wednesday, “hump day” to many but traders often refer to it as “drive day” as the market finally decides where it’s headed, this time the market enjoyed broad based buying with over 80% of stocks closing in positive territory, the index scaled fresh 3-week highs as Omicron fears seemed to vanish almost as fast as they arrived. The 1.25% gain took the local market within 3% of its all-time high only a few weeks after the doom and gloom merchants were focusing on either bond yields or Omicron. I feel this is an ideal time to remember some seasonality factors and simple statistics with only 16-days left before Christmas:

- If we assume (dangerous word) that 7168 is the low for this December we could easily see 7500-7600 in the coming weeks just through simply extrapolation of the average monthly ranges post COVID.

- We all know the bullish statistics around Christmas e.g. Over the last 40-years the ASX has rallied 85% of the time from mid-December until January delivering an average return of 2.9%.

- Also the influential Banking Sector has rallied 100% of the time since 1992 with an average return of 7% i.e. a potentially huge tailwind for the ASX.

Overall there’s nothing new here, MM is still bullish targeting the 7700-7800 area into early 2022 i.e. another 4-5% rally although higher levels cant be ruled out as the trends clearly up. The important factor to remember is MM are fully committed to stocks, as we basically have been since the start of the pandemic, with our Flagship Growth portfolio only holding 1% in cash – if it was a game of poker we would be all-in! Hence our next strategic move will be to de-risk into anticipated strength i.e. we could comfortably see ourselves taking cash levels significantly higher in Q1 of 2022 while we reassess what comes next as interest rates start to rise.

US equities were mixed overnight with weakness in the financials potentially going to weigh on our index early on, the SPI futures are calling the ASX200 to open down around 0.4% this morning not helped by a likely 50c dip by BHP Group (BHP) to start the day.

MM remains bullish the ASX targeting fresh highs into 2022

Add To Hit List

If we are correct and the local market continues to rally into 2022 we intend to become especially focused on our current holdings over the coming weeks – tis the time to be merry and boring!