Tuesday saw the ASX200 rally strongly finally closing up just shy of 1% on broad based buying with strong gains enjoyed by most pockets of the market, however the standout performances largely came from stocks who were whacked in previous sessions around Omicron fears, as we’ve said over recent days the new variant emanating from South Africa doesn’t appear to be an economic or health game changer, the RBA concurs with our feeling here believing the Omicron variant is a source of uncertainty but no major risk to our economy. Overall the Australian central bank gave the ASX a very welcome boost yesterday afternoon:

- The RBA believes that Omicron is nothing more than anther speed bump in our exit from the pandemic with rising inflation the defining factor on when interest rates will increase.

- The overnight cash rate was held at 0.1% on Tuesday and Philip Lowe still doesn’t anticipate rate hikes until 2023 at the earliest going by his inflation outlook – the RBA is “prepared to be patient” before lifting interest rates.

- Surprisingly the RBA have maintained their bond buying program until at least mid-February, they appear keen to let markets adjust gradually to the normalisation of interest rates – markets are pricing in a hike next July and a full 1.75% by the end of 2023.

The Australian Dollar continued to rally after the RBA’s comments, at MM we’re sticking to our view that the 70c level will hold the pullback from its February high implying the $US earners may struggle whereas the commodities and especially precious metals should enjoy a tailwind – we are positioned accordingly across our portfolios. Over the last 2-months we’ve experienced significant volatility courtesy of both soaring short-term bond yields and the Omicron variant, what’s next? My “gut feel” is no fresh news only a strong Santa rally to end 2021 and extend the post COVID bull market.

The headlines this morning in the AFR are leading with Treasurer Josh Frydenberg looking to regulate the likes of BNPL stocks, this should prove an interesting test for the likes of Zip (Z1P) which bounced almost 10% yesterday.

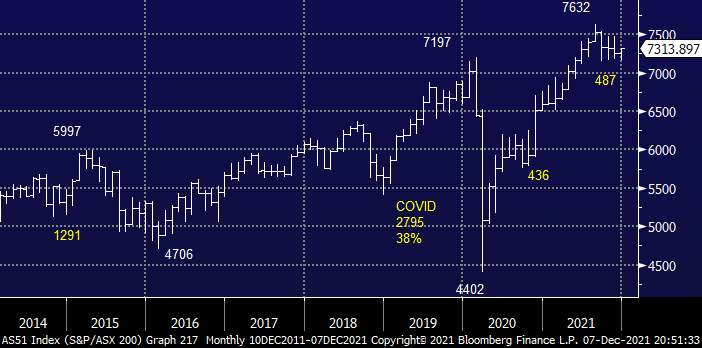

Overnight US stocks extended their weekly gains with the S&P500 rallying 1.77% as the large tech stocks came back into favour, encouragingly the SPI’s pointing to an open around 7350 this morning for the ASX200 and if we’re correct the surprises should now be on the upside as we head into Christmas and 2022 – when we look at the chart of the local market post COVID the last 5-weeks simply appears like a correction within an underlying rally with fresh highs looming on the horizon.

MM is bullish the ASX into 2022 targeting fresh highs

Add To Hit List