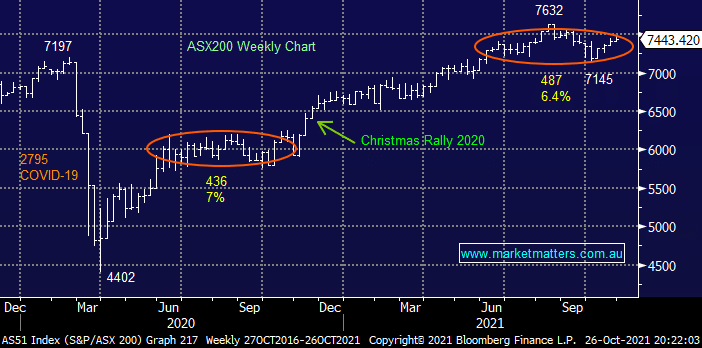

The ASX200 again tried to push higher early on Tuesday only to drift through the afternoon, this style of price action might often concern us but the local market just feels a little stretched this month, we still anticipate fresh highs into November / Christmas. All the action on Tuesday was on the stock / sector level as lithium stocks rallied while gold stocks gave back some of their recent gains but overall it was a quiet day as we see slowly & quietly say goodbye to October.

Australian bond yields and the $A keep grinding higher with the local currency now up 4c against the $US since late August, if we are correct overseas holidays should be cheaper in 2022, at least with regard to spending money. However as we’ve said previously this is old news unless we witness another surge higher & / or the RBA performs an about face and starts hiking interest rates – we don’t expect either before Christmas. Yesterday we mentioned that gold stocks are one of our picks for a countertrend recovery over the coming months another thought we’re mulling over is deep discounted stocks which offer plenty of value on more traditional models – see tomorrows report.

Interestingly most people I speak to are still worried about equity markets although very few are actually selling while even less are proclaiming it to be cheap and the best buy since sliced bread. Nothing overly surprising here as human emotion steers us to sell a rising market and buy one that’s falling, unfortunately the statistics tell us the reverse pays dividends over time. For now MM will stay long but our “3 steps forward 2 back” outlook into 2022 still suggests that reducing exposure into strength is prudent. Interestingly the latest BofA Fund Managers survey showed us the feelings of professionals are pretty much aligned with my feedback from retail investors as 2021 comes to an end:

- Fund managers are their least bullish since 2020 with inflation now their greatest concern.

- Cash levels are now at a 12-month high as inflation & China weighs on confidence.

- The speculative positioning in the S&P futures remains net short, we believe it’s very unlikely to see this bull market topping out with a net short position, its actually more likely to continue to squeeze ever higher – the path of most pain!

If both retail and professional investors are bearish stocks we are happy to be long albeit remaining cautious as some of our targets loom on the horizon.

Overnight US stocks rallied enjoying broad based gains to send indices close to all-time highs following strong earnings from General Electric (GE US) and United Parcel Service (UPS US) although Facebook (FB US) missed forecasts sending the stock down over 4% – the big guns have also reported this morning i.e. Alphabet (GOOGL US), Microsoft (MSFT US) and Twitter (TWTR US). At this stage the SPI futures are calling the local market to open slightly higher this morning but this will undoubtedly be influenced by these results.

MM remains bullish the ASX targeting fresh highs in the weeks / months ahead

Add To Hit List