The ASX200 continues to struggle to advance much above 7400 as it pays respect to the historical statistics in play i.e. the bulls may have to wait until the Melbourne Cup runners are off and running before we can see a sustained challenge on 7500, and above. Yesterday saw the index drift from its lunchtime highs in sympathy with US futures, the COVID re-opening names experienced further profit taking while the Real Estate Sector was the standout top performer.

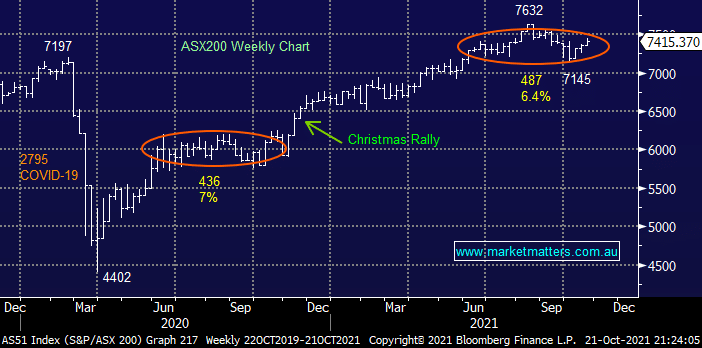

Its important not to get lulled into a slumber by the ASX after more than 20-weeks of sideways action, a quick glance at the charts shows how similar the current price action is to this time last year, just before the market surged 12% into Christmas i.e. its time for a cold shower, coffee and to be alert. The local index might be showing no obvious signs that new all-time highs are just around the corner but when we consider how it’s shrugged off the likes of China Evergrande, COVID, soaring bond yields and a collapsing iron ore price I “wouldn’t be short for quids”.

The banks very often lead the rally into Christmas helped by investor appetite for 3 of the big 4 trading ex-dividend in November but it might be a touch harder for them to carry the torch this year as the yield curve has flattened dramatically over recent weeks i.e. banks borrow short and lend long, in other words they prefer the exact opposite scenario to what we’ve seen over recent months:

- Banks margins are squeezed for example if they have to pay increasing interest rates on term deposits but mortgage rates do not rise at the same speed I.e. the gap narrows as does their profitability.

- We need to see a change in perception around inflation i.e. that recent increases are not just transient before longer dated yields rise / play catch up alleviating this margin pressure.

- Hence this time we may need some strong results from ANZ., NAB and Westpac to ignite the sector although I would again note they’ve been extremely resilient in the face of a flattening curve, which implies underlying strength.

Overnight US stocks had a mixed session with tech stocks rallying while the resources struggled, the net result locally is the SPI futures are calling the ASX200 to open flat although a $1 drop by BHP in the US is likely to make it hard going on the upside.

MM remains bullish the ASX targeting fresh highs in the weeks / months ahead

Add To Hit List