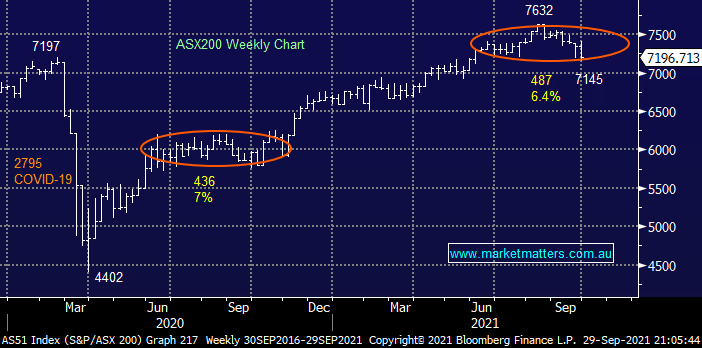

As we approach Q4 the question being asked by many is can the AX200 again rise from the ashes, yesterday it was battered for the 2nd successive day as September looks set to live up to its bearish reputation, the index is sitting down 4.5% with just today’s session remaining. Stocks have been caught with a classic “1-2 combination” as the deteriorating macro picture threatens to derail the liquidity driven bull market:

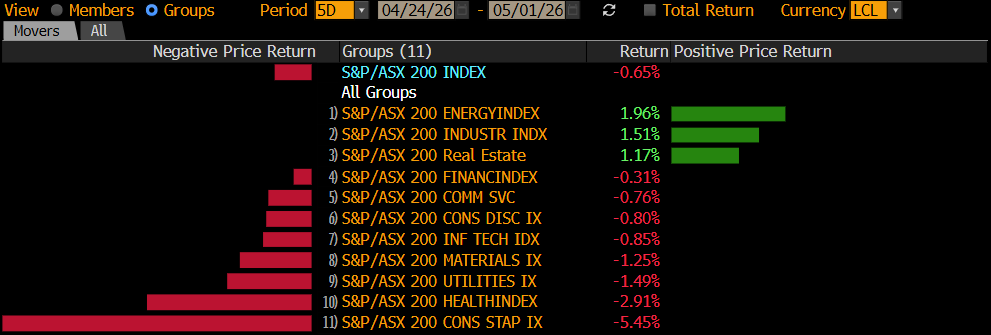

- Firstly we had the China Evergrande debt crisis which looks set to curtail the runaway Chinese property market which in turn has led to iron ore prices plunging dragging with it influential local names such as BHP Group (BHP), RIO Tinto (RIO) and Fortescue Metals (FMG).

- Secondly bond yields have stealthily advanced to their highest level in 3-months as the surging oil price has reignited global inflation fears, a move that has created a major headwind for the likes of Healthcare and Tech Sectors.

This time last year the market fell in a very similar manner, todays 6.4% retracement is actually still a touch light compared to the one in 2020. At this stage we see no reason to alter our bullish roadmap into Christmas but if important sectors like the iron ore names feel likely to have already topped for the foreseeable future then some major heavy lifting appears required by a diminishing number of stocks – a typical characteristic of a stock market top.

One bullish aspect from Wednesday was yet another takeover bid, this time we saw US-based investment firm TPG Global make a conditional $10.35 bid for Smart Group (SIQ), a premium of over 30% to where the stock opened on Tuesday. This would clearly appear to be a deal the suitor is keen to complete although the stock closed yesterday at a 11.5% discount to the offer which probably reflects the number of deals that have ultimately failed in 2021 – we like the risk reward towards SIQ at yesterdays close and are thus staying long in our Active Income Portfolio. The clear positive takeout for the ASX is buyers are still circling in those hills, we may even see a short-term run of deals as the cost of debt threatens to rise.

Overnight US stocks were mixed but at least not weak, the S&P500 bounced 0.3% while the tech based NASDAQ still closed marginally lower, the SPI futures are calling the local market to open up around 20-points in what feels like being a quiet end to a fairly volatile September.

MM remains bullish the ASX targeting fresh highs in the weeks / months ahead

Add To Hit List