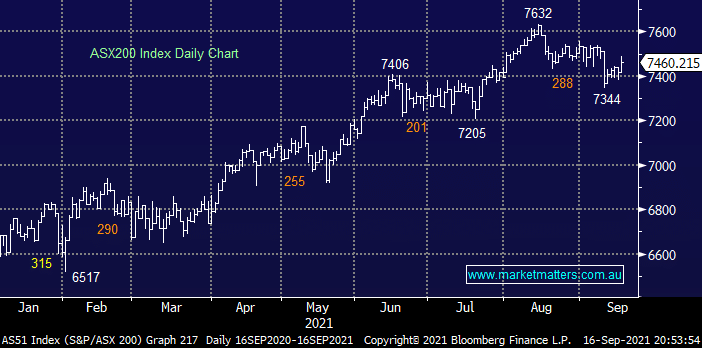

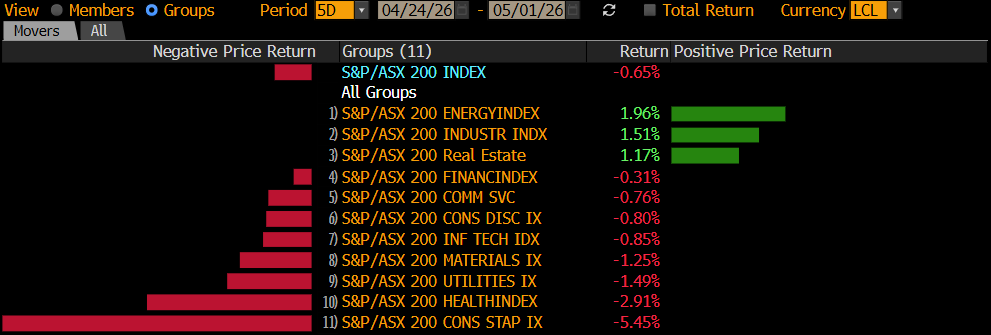

The ASX200 rallied strongly yesterday as it enjoyed broad-based buying, by 4pm 60% of the index had closed in positive territory with the Energy Sector again best on ground following the strong rally by crude oil. Outside of iron ore names which have seen the likes of Fortescue Metals Group tumble 35% in just 8-weeks, although it did pay a major dividend on route, the broad market has been devoid of any meaningful selling as we continue to hover within a few percent of its all-time high.

Scott Morrison’s nuclear sub deal with the US & UK feels destined to undermine our already fragile trading relationship with China and with the iron ore price crashing almost 50% since mid-May we feel increasingly less important to the Asian powerhouse. Stocks with a dependency on Chinese trade have remained anchored to the losers corner through recent times and its now hard to imagine this improving pre-Christmas e.g. Treasury Wine (TWE), a2 Milk (A2M) plus the likes of RIO Tinto (RIO) & Fortescue (FMG) since the demise of iron ore.

Earlier in the week the Bank of America Fund Managers Survey delivered few surprises, more a case of reaffirmation of recent trends:

- The Delta Variant has sent growth expectations down to their lowest level since April 2020 – just before bond yields and equities started a strong 12-month advance.

- Downside protection to stock declines are at their lowest levels since January 2018 – just before a short sharp 12% correction.

- Cash levels edged up to 4.3% from 4.2% although the number of managers who are increasing levels of risk has increased.

Overnight US stocks bounced around ahead of Fridays “Quadruple Witching Hour” this interesting named phenomenon is when markets index futures & options expire along with individual stock options & futures – usually a volatile session for markets, especially in the last hour. The SPI Futures are looking for a marginally lower open today for the ASX although it feels a touch optimistic after the resources were smacked in the US as the Greenback enjoyed a strong session e.g. BHP is set to open down 80c, back under $40 for the first time since mid-April.

MM remains bullish the ASX and a keen buyer of pullbacks

Add To Hit List