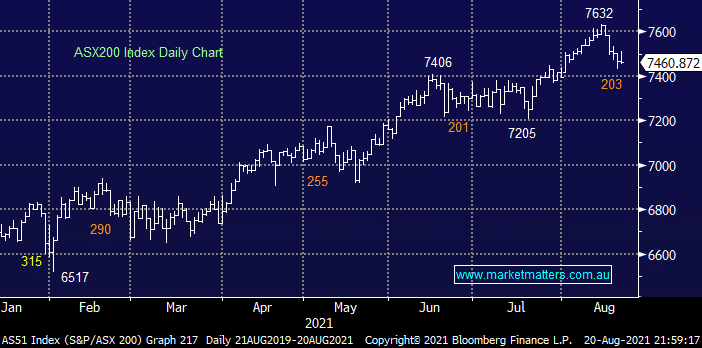

The ASX200 endured a rare fall last week with the heavyweight Resources and Banks inflicting the damage, interestingly under the hood the stock and sector performance was very mixed with a number of shining lights from some less influential stocks. There was some eye catching declines by many major names from within the Value Sector which created a meaningful headwind for the local index, arguably the ASX fought well to only drop -2.2%:

- Banks – Bendigo Bank (BEN) -11.7% and Commonwealth Bank (CBA) -4.6%.

- Iron Ore names – Fortescue Metals (FMG) -8.7% and RIO Tinto (RIO) -10.9%.

- Copper stocks – OZ Minerals (OZL) -9.5% and Sandfire Resources (SFR) -13.4%.

- Nickel Stocks – Nickel Mines (NIC) -12.7%.

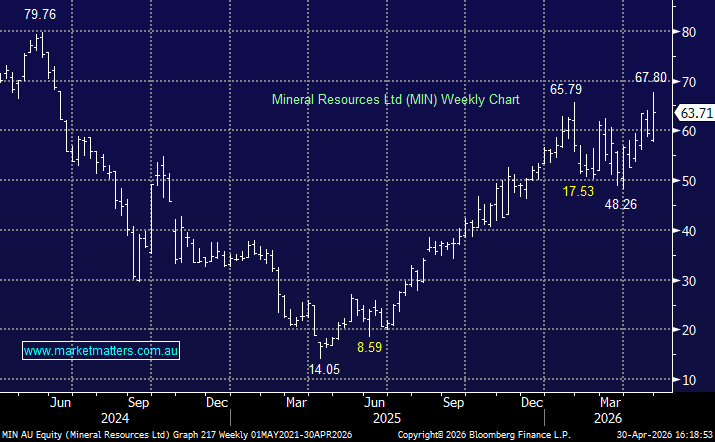

- Lithium stocks – Mineral Resources (MIN) -17% and Orocobre (ORE) -8.9%.

- Energy stocks – Woodside Petroleum (WPL) -11.2% and Beach Petroleum (BPT) – 11.2%.

- Diversified Miners – BHP Group (BHP) -16% and South32 (S32) -7.6%

The plunge which rolled through the resources stocks was triggered by a couple of macro events, including a firmer $US triggering falls in most commodity prices and concerns around Chinas economic growth moving forward, to add spice to the fire the press are running stories such as “China is pulling the plug on iron ore”. However a quick look at the damage inflicted on our Materials Sector illustrates there was nowhere to hide as sellers unceremoniously dumped stocks exposed to a deterioration in global growth courtesy of the Delta Variant – we’ve been flagging this but the aggressive nature of the sectors delayed take-up on the theme surprised us.

China will ultimately determine commodity prices into and through 2022 and importantly Beijing has shown signs in recent months that it’s still prepared to press the stimulus button. Xi Jinping et al have a balancing act on their hands as they look to implement an emission reduction strategy while maintaining a decent degree of growth which their people now expect. MM remains committed to its reflation outlook moving forward and believe the current dip in the Resources Sector is a buying opportunity (we’ve been targeting this for a few months), medium / longer-term we prefer the likes of copper, nickel and lithium to iron ore / oil but as we’ve enjoyed with Whitehaven Coal (WHC) the ESG investment movement has created some phenomenal opportunities in the oversold fossil fuel space.

Following a solid bounce in the US on Friday the SPI futures are pointing to a firmer opening this morning with interest rate sensitive stocks likely to lead the recovery e.g. Tech and the “yield play names”.

MM remains bullish equities and a buyer of weakness, primarily in the value stocks

Add To Hit List