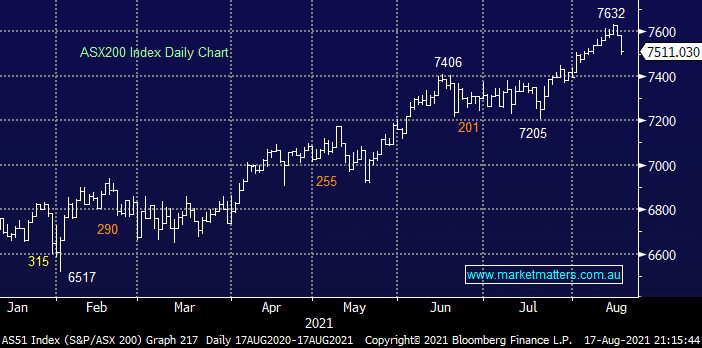

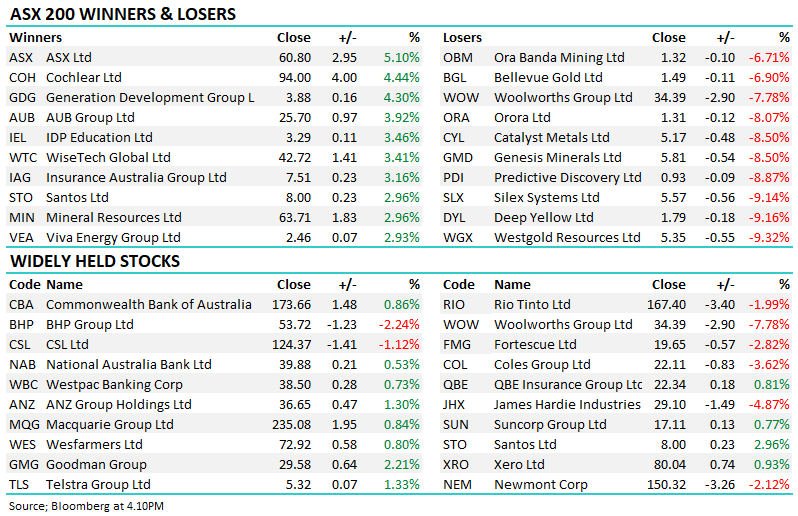

The ASX200 experienced it’s worst day in 2 months yesterday finally closing down 71-points as the banks and resources again fell as confidence continues to wane towards the global economy. The RBA echoed the markets concern that the Delta Variant might push Australia back into a recession as they considered further stimulus during their August board meeting– “The board would be prepared to act in response to further bad news on the health front should that lead to a more significant setback for the economic recovery”. This change in rhetoric / mindset illustrates why investors must remain openminded as we never know exactly what’s around the corner.

The market has a habit of knocking complacent investors and that’s also been the case over the last 48-hours with regards to reporting season as misses have dominated the news, just as investors were becoming increasingly confident that corporate strength could withstand the current painful lockdowns across Australia. The dominant movers have been on the downside this week even while there have been a few solid beats thrown into the mix:

- Tuesday saw Magellan (MFG) -10.2% and Sims Group (SGM) -3% both fell after reporting earnings.

- Monday saw Beach Petroleum (BPT) and Bendigo Bank (BEN) both fall almost 10% after they reported earnings.

- This morning BHP Group (BHP) is set to open down -6.2% after reporting aftermarket yesterday, they delivered a -2.2% miss on the NPAT front plus a petroleum demerger, potash development/approval & the unification of their UK structure – bigger picture we like the companies direction however a lot to unpack here.

US stocks endured their worst drop in a month overnight on concerns that COVID will hinder the global economic recovery, a theme that’s picking up momentum around the world – poor US Retail Sales overnight helped dampen optimism. The SPI Futures are calling another -0.5% fall early this morning although it was looking much worse around 2am before US stocks recovered half of their intra-days losses. The look and feel of stocks has changed this week and markets finally feel vulnerable to a decent pullback within the liquidity driven bull market.

MM remains bullish the ASX and keen buyers of pullbacks

Add To Hit List