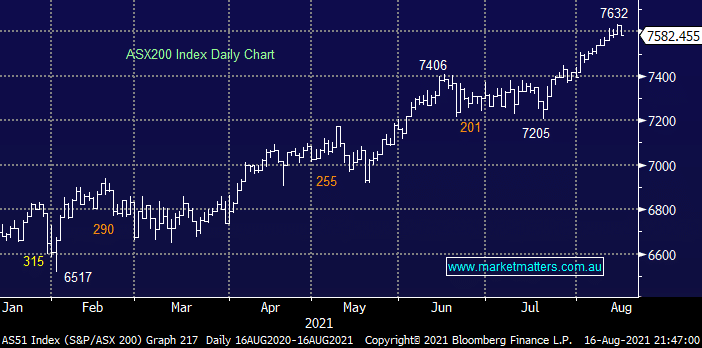

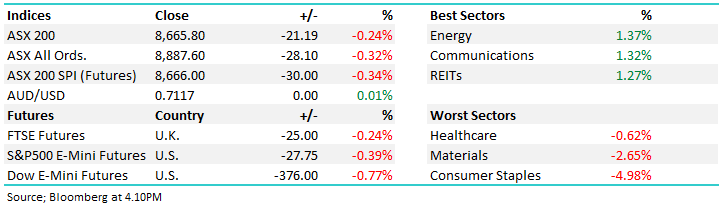

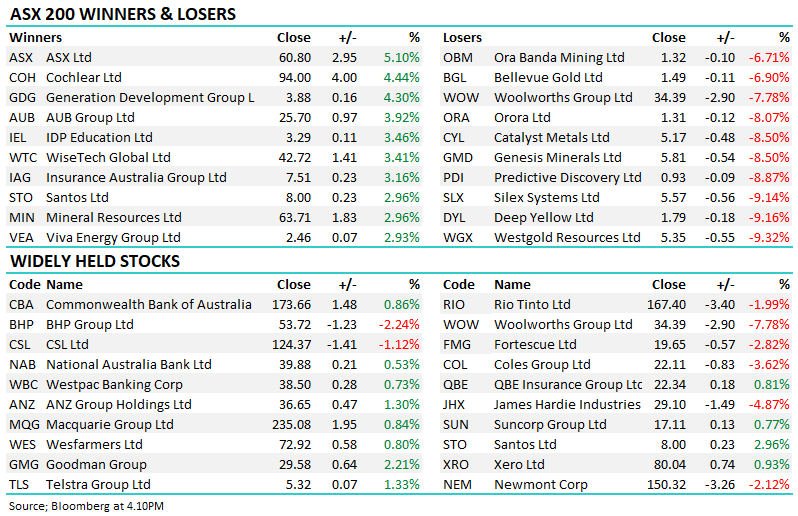

The ASX200 struggled yesterday as the two most influential sectors fell in tandem, Bendigo Bank (BEN) -9.9% led the Banking Sector lower while OZ Minerals (OZL) -3.9% took line honours for the major miners. The index itself fell only -0.6% although the selling felt more aggressive with 11 companies falling by over 4% while only one rallied by the same degree. A couple of stocks which we hold in our Growth Portfolio and are hoping to add into weakness were on the receiving end of the markets wrath on Monday but unfortunately none are yet close to our buy zone e.g. OZL and Santos (STO).

Mondays weakness was sparked by a rare day of more misses than beats on the earnings front combined with another day of record COVID cases for Sydney plus a weak overnight session for US futures & Asian indices, all things considered a drop of just 0.6% was good effort. We feel volatility is due to rise over the coming weeks although we’ve been wrong on that front before in 2021 – this time we have got reporting season and COVID on our side, fingers crossed we’re correct because volatility is usually accompanied by opportunity.

Broader financial markets followed the lead from stocks yesterday with both bond yields and the $A falling towards their recent lows as the Delta Variant puts the economic recovery on ice. The latest data from both the US and China have been soft which feels like its caught a few recovery bulls wrong footed. If we are correct and both are poised to break their recent lows the likelihood is that the banks and resources will continue yesterday’s underperformance, a move we intend to fade through August / September.

Overnight US stocks reversed losses during our time zone to record their 49th record close for the year, gains were led by the interest rate sensitive Healthcare and Utility Sectors as bond yields continued their drift lower, market heavyweight Apple Inc. (AAPL US) also posted fresh all-time highs. Elsewhere Tesla (TSLA US) fell -4,3% as the US commenced an investigation into its Autopilot crashes, ongoing weakness in the banks and resources continued to weigh on the SPI Futures which are only pointing a slightly higher open, not helped by an equivalent 40c drop by BHP Group (BHP) in US trade.

MM remains a buyer of weakness across most stock market sectors

Add To Hit List