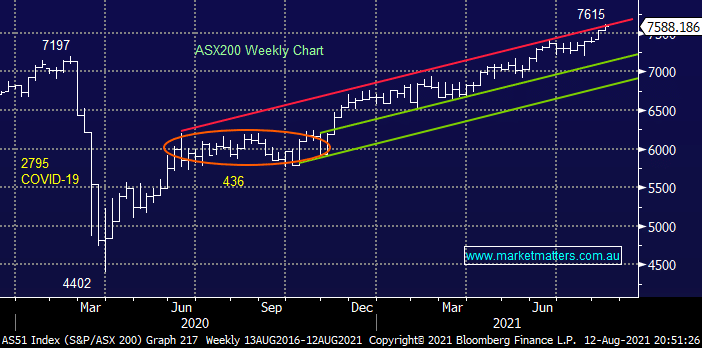

The local market struggled to hold onto early gains yesterday as profit taking hit Commonwealth Bank (CBA) and the IT Sector, it felt like a weak day although we still managed to close marginally higher. Stock rotation was prevalent within the ASX200 yesterday as 15 stocks rallied by 3% or more, while 6 companies fell by the same degree, as we’ve flagged in a number of reports MM believes this will be opus operandi into Christmas, and probably well into 2022. Elsewhere across Asia, equities were on the back foot illustrating the impressive resilience being demonstrated by local equities towards any bad news, large or small.

MM reduced our exposure to the banks on Thursday through trimming our holdings in both CBA and NAB, arguably just when things look great. However, we went long during the royal commission through a deluge of adverse publicity plus a number of subscriber questions doubting our logic but as famous investor Baron Rothschild said “Fortunes are made by buying low and selling too soon”. Lets consider a few brief facts around the banks today:

- The RBA has lent the Australian banks $188bn at just 0.1% until 2024.

- CBA’s yield has now fallen from well over 5% to nearer 3% today as their surplus cash drops from $11.5bn to $7.5bn.

- NAB raised $1.25bn in just April 2020 below book value at $14.15, now they’re buying back stock at ~$27 at 1.4x book value – good business?

Obviously things look great for the banks today, almost a polar opposite to how bad they did during COVID and the ill-fated Royal Commission but given valuations now, we believe its time to trim our holdings, even if we indeed believe they will probably get dragged higher by todays relentless bull market – the banks are starting to have that “as good as it gets” feel about them especially considering how much money the RBA has donated to their cause.

Australian bond yields followed their US peers lower yesterday on the back of the more benign US inflation data on Wednesday night, we might have been a touch premature calling a swing low in bond yields with the COVID picture continuing to deteriorate but we still believe they are at least “looking for a low” as MM likes to say. Interestingly as bond yields drifted value stocks rallied and growth fell, the opposite to the historical playbook implying that equities don’t envisage a meaningful drop in yields from today’s levels after their relentless push lower since February.

Overnight US equities were quiet with some minor reversion back towards the tech names, the S&P500 ultimately closed up +0.3% at its 47th record close for 2021. I read an interesting comment this morning out of Goldman Sachs which flows on from our report yesterday – “Equities become the proverbial term – there is no alternative – and that ultimately is a money flow story”. The SPI Futures are pointing to a solid +0.4% open this morning, to challenge its all-time high – with BHP Group (BHP) falling in the US there’s obviously anticipation for a much better session by the Financials.

MM remains a buyer of weakness across most stock market sectors

Add To Hit List