Which stocks benefit from the expectant domestic tourism boom?

**This is an extract from the Market Matters Morning Report from 15 May. Click here to get access to the full report and more

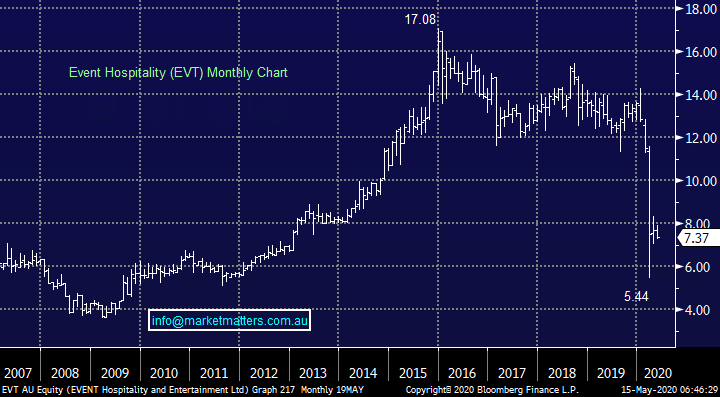

1 Event Hospitality (EVT) $7.37

Cinema operator EVT is a Sydney based $1.2bn business that has been significantly impacted by COVID-19 and will continue to be so while social distancing remains but having picked up the kids from school this week I feel this is already relaxing in a major way, rightly or wrongly. Scott Morrison's “Step 2” to re-open Australia includes cinemas although details around how many patrons will be allowed at one time will define potential profitability, or not.

The company was under performing over the last 5-years which doesn’t excite me, but it is a business that should find switching the lights back on fairly straightforward. We see value in EVT around current levels especially as this has been an excellent reliable dividend payer over the last 5-years, EVT is a potential “outside of the box” yield play moving forward.

MM is neutral / positive EVT.

Event Hospitality (EVT) Chart

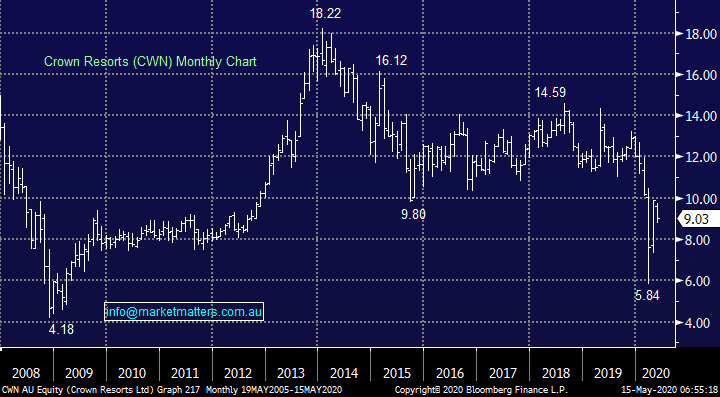

2 Crown Resorts (CWN) $9.03

Obviously CWN is best known for its casinos and looming new build at Barangaroo in Sydney but it also operates hotels, shops, restaurants and even Betfair Australasia although its revenue is really all about gambling on the tables. Revenue from locals will never match those from gambling loving Asia but if they can keep the “lights on” until things return to normal CWN trading sub $10 is likely to look cheap in years to come. It also helps that private equity business Blackstone recently took a 9.99% stake in the business at $8.15, corporate action might well be on the horizon.

The growth of ethical investing funds which we’ve discussed over recent months is a headwind for the stock and should not be underestimated, the likely impact is P/E (valuation) contraction in the years ahead but not necessarily price if the underlying business performs.

MM likes CWN around current levels.

Crown Resorts (CWN) Chart

2 Crown Resorts (CWN) $9.03

Obviously CWN is best known for its casinos and looming new build at Barangaroo in Sydney but it also operates hotels, shops, restaurants and even Betfair Australasia although its revenue is really all about gambling on the tables. Revenue from locals will never match those from gambling loving Asia but if they can keep the “lights on” until things return to normal CWN trading sub $10 is likely to look cheap in years to come. It also helps that private equity business Blackstone recently took a 9.99% stake in the business at $8.15, corporate action might well be on the horizon.

The growth of ethical investing funds which we’ve discussed over recent months is a headwind for the stock and should not be underestimated, the likely impact is P/E (valuation) contraction in the years ahead but not necessarily price if the underlying business performs.

MM likes CWN around current levels.

Crown Resorts (CWN) Chart

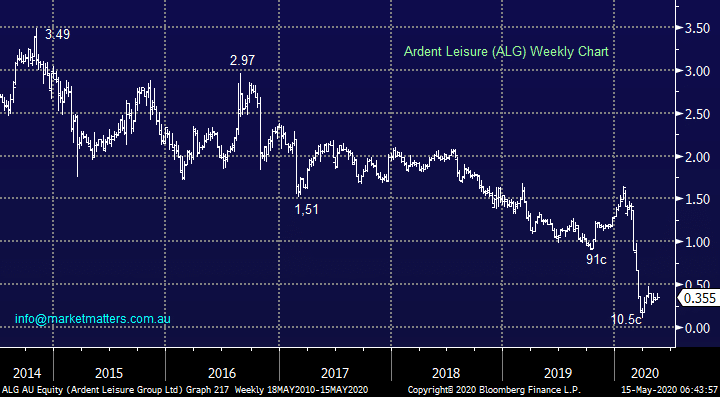

3 Ardent Leisure (ALG) 35.5c

ALG has been struggling big time since the Dreamworld disaster but the forced change in holiday destinations might just give the amusement park operator a much-needed new lease of life – remember Disney re-opened in China this week. Unfortunately, in February the inquest into the Thunder Rapids ride found the parks systems were “frighteningly unsophisticated” – this sounds very expensive moving forward.

I have friends who have been to both Disneyland and Dreamworld in the last few years and they regard the later as being akin to a local suburb playground from a comparative basis. However, Whitewater World and Sky Point Observation Deck are better assets, it just needs to get Dreamworld sorted once and for all without legal and operational costs dragging the business under.

MM is neutral ALG – all seems a bit hard

Ardent Leisure (ALG) Chart

3 Ardent Leisure (ALG) 35.5c

ALG has been struggling big time since the Dreamworld disaster but the forced change in holiday destinations might just give the amusement park operator a much-needed new lease of life – remember Disney re-opened in China this week. Unfortunately, in February the inquest into the Thunder Rapids ride found the parks systems were “frighteningly unsophisticated” – this sounds very expensive moving forward.

I have friends who have been to both Disneyland and Dreamworld in the last few years and they regard the later as being akin to a local suburb playground from a comparative basis. However, Whitewater World and Sky Point Observation Deck are better assets, it just needs to get Dreamworld sorted once and for all without legal and operational costs dragging the business under.

MM is neutral ALG – all seems a bit hard

Ardent Leisure (ALG) Chart