The majority of companies have now reported and while we hate using the old cliché, its been better than feared, much like the broader economic outcomes that have played out over the past year which has prompted a more aggressive stance by central banks globally – the imminent recession is getting less airtime and markets are reflecting that. As we’ve written at nauseum over recent months, we’re neutral at the index level but that belies significant action that’s unfolding under the hood, a theme we expect to continue, creating a great environment for stock picking, as long as you pick the right stocks!

A solid session to kick off the new week despite a mixed bag on the reporting front as we transition down the market cap spectrum over the next week. So far, results have been better-than-expected with earnings beats outnumbering misses 5:3, however there is growing uncertainty around what comes next and that’s filtering into softer guidance in aggregate for FY24, prompting downgrades.

The worst of it was seen in early trade today with the ASX off ~100pts at the lows, but some buyers emerged throughout the session, particularly amongst the recently weak Staples while Healthcare stocks also attracted some attention from early lows, Ramsay Healthcare (RHC) for example rallied 3% from the depth of despair this morning! It felt like a tough week, and given only 2 sectors finished in the black, the selling was fairly broad-based, however, it was far from aggressive (ASX -0.5% for the week) and there were plenty of stocks that did well.

A solid session for the ASX today, although some late selling again took some of the sheen off the day. IT stocks continued on a volatile week where ~5% swings have become commonplace, while the results today ensured some big moves under the hood, unfortunately for Market Matters, we were on the wrong side of a couple today!

Early weakness didn’t last long as resources helped support the index as it rallied throughout the morning. At its best, the ASX was up 0.75% with the bulls looking to regain the ascendancy following fresh 5-week lows set yesterday. Sellers did appear as the market was closing, shaving about half of the gains from the index in the last few hours. Another big day for reporting is in the books as the mixed fortunes of reporters continue.

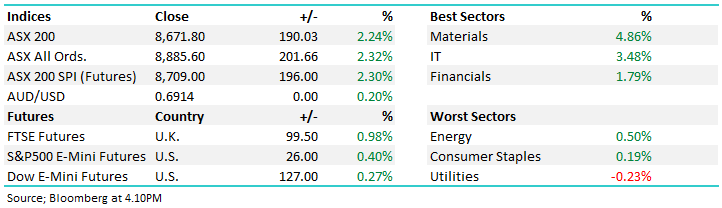

The ASX 200 bounced today as generally better than expected earnings, particularly from some key technology stocks reinvigorated the bulls, despite BHP slightly underwhelming.

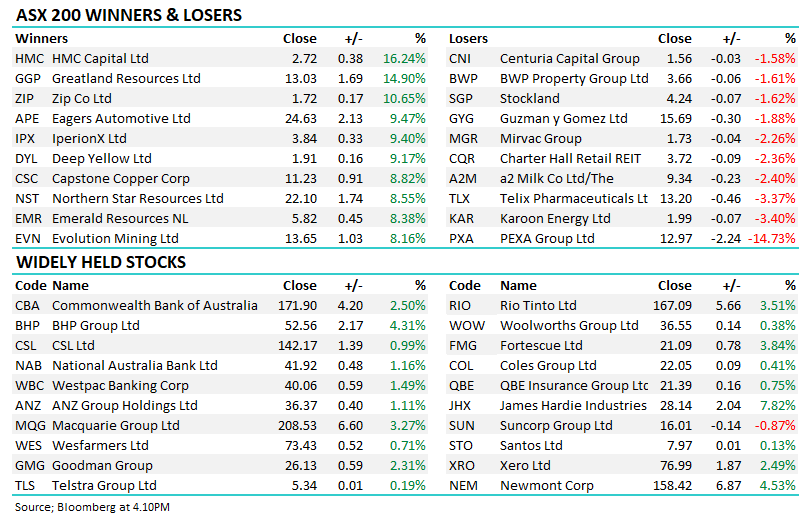

A soft start to the new trading week which sees the vortex of local company results with the next 3 days seeing a significant number of company updates. There was certainly volatility at the stock level today with Iress (IRE) -35% & A2 Milk (A2M) -13.56% on the wrong side of it, while strong updates from Premier Investments (PMV) +12.23% and Breville (BRG) showed there is life left in retail!

A flat end to a tough week for markets with a lot to digest: Better US data drove bond yields higher, China property concerns as news of defaults linger pushed miners lower, while local reporting underpinned rising volatility across the board. Phew, it’s Friday!

The ASX fell again today, although some obvious ‘dip buying’ came to pass as reporting season continued to build, while a higher unemployment rate provided further evidence to support a continued RBA pause.

Weakness across international equity markets bled into the ASX today with shares trading to a 4-week low. The US market struggled following better-than-expected retail sales prints leading to upwards pressure on rates. This compounded concerns around China’s property market and economic growth outlook which has weighed on equity markets across the region in recent weeks, yesterday’s rate cut from the PBOC only providing short-term relief. Reporting season is now well and truly in full swing while CBA went ex-div today adding to the red on the index.

A solid session to kick off the new week despite a mixed bag on the reporting front as we transition down the market cap spectrum over the next week. So far, results have been better-than-expected with earnings beats outnumbering misses 5:3, however there is growing uncertainty around what comes next and that’s filtering into softer guidance in aggregate for FY24, prompting downgrades.

The worst of it was seen in early trade today with the ASX off ~100pts at the lows, but some buyers emerged throughout the session, particularly amongst the recently weak Staples while Healthcare stocks also attracted some attention from early lows, Ramsay Healthcare (RHC) for example rallied 3% from the depth of despair this morning! It felt like a tough week, and given only 2 sectors finished in the black, the selling was fairly broad-based, however, it was far from aggressive (ASX -0.5% for the week) and there were plenty of stocks that did well.

A solid session for the ASX today, although some late selling again took some of the sheen off the day. IT stocks continued on a volatile week where ~5% swings have become commonplace, while the results today ensured some big moves under the hood, unfortunately for Market Matters, we were on the wrong side of a couple today!

Early weakness didn’t last long as resources helped support the index as it rallied throughout the morning. At its best, the ASX was up 0.75% with the bulls looking to regain the ascendancy following fresh 5-week lows set yesterday. Sellers did appear as the market was closing, shaving about half of the gains from the index in the last few hours. Another big day for reporting is in the books as the mixed fortunes of reporters continue.

The ASX 200 bounced today as generally better than expected earnings, particularly from some key technology stocks reinvigorated the bulls, despite BHP slightly underwhelming.

A soft start to the new trading week which sees the vortex of local company results with the next 3 days seeing a significant number of company updates. There was certainly volatility at the stock level today with Iress (IRE) -35% & A2 Milk (A2M) -13.56% on the wrong side of it, while strong updates from Premier Investments (PMV) +12.23% and Breville (BRG) showed there is life left in retail!

A flat end to a tough week for markets with a lot to digest: Better US data drove bond yields higher, China property concerns as news of defaults linger pushed miners lower, while local reporting underpinned rising volatility across the board. Phew, it’s Friday!

The ASX fell again today, although some obvious ‘dip buying’ came to pass as reporting season continued to build, while a higher unemployment rate provided further evidence to support a continued RBA pause.

Weakness across international equity markets bled into the ASX today with shares trading to a 4-week low. The US market struggled following better-than-expected retail sales prints leading to upwards pressure on rates. This compounded concerns around China’s property market and economic growth outlook which has weighed on equity markets across the region in recent weeks, yesterday’s rate cut from the PBOC only providing short-term relief. Reporting season is now well and truly in full swing while CBA went ex-div today adding to the red on the index.

Check your email for an email from [email protected]

Subject: Your OTP for Account Access

This email will have a code you can use as your One Time Password for instant access

Verication email sent.

Check your email for an email from [email protected]

Subject: Your OTP for Account Access

This email will have a code you can use as your One Time Password for instant access

!

Invalid One Time Password

Please check you entered the correct info, please also note there is a 10minute time limit on the One Time Passcode

To reset your password, enter your email address

A link to create a new password will be sent to the email address you have registered to your account.

Market Matters members receive daily market reports, real-time trade alerts, full access to 5 portfolios and dynamic company data.

Choose how you'd like to proceed:

We have a range of membership options to suit your needs and budget, why not join today and get unlimited access to the premium Market Matters service.