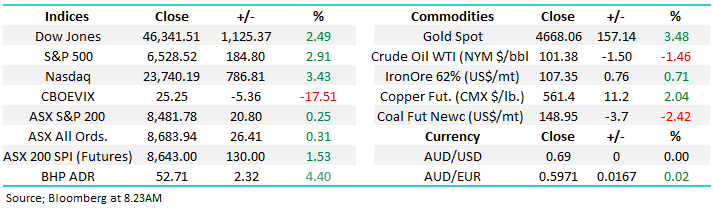

Some signs of buying helped support the local market today, driven in particular by the heavy-weight sectors of Materials and Financials. The support there helped put an end to a 3-day rout which had set the ASX200 to an 11-month low. Locally, the focus will turn to inflation data due out tomorrow morning, the next print to determine where rate expectations head in the short term.

Further pain was felt across the ASX today as the risk-off trade continued in the face of rising geopolitical tensions. Commodity markets took a hit, flowing through to local Materials and Energy stocks with the weakness today sending the index to an 11-month low. The recent underperformers from a sector perspective were the relative outperformers today, healthcare and Staples bucking the trend to close higher.

The ASX caught a cold from the weakness seen in the US overnight. Selling came on the back of Fed Chair Jerome Powell’s hawkish comments which sent to the US 10-year rate to 16-year highs, just a shave shy of 5%. Further tensions in the Middle East also weighed on growth assets, though that was supportive of Energy and Precious Metals, two areas of the market that largely bucked the trend today. The ASX200 fell -150pts/-2.13% during the week.

A tough day at the office for the ASX, tracking weakness in US/European markets that permeated across Asia. More tension in the Middle East is threatening higher Oil prices that would underpin persistent inflation and higher interest rates, all very logical and these concerns have pushed the ASX 200 back down to the bottom of its recent trading range.

A choppy but overall positive session at the index level, although there was a lot happening under the hood, with some hits and a few big misses to get across today.

The ASX had a positive session, although finished ~40pts below the highs after the latest RBA minutes showed another rate hike is not off the table. The list of today’s winners is an eclectic bunch with one thing in common, most have had a horrible last 12-months, perhaps some bargain hunting might be about to emerge.

A lacklustre session locally with a smorgasbord of uncertainty playing into investor minds, a -0.35% fall was okay considering the news flow. Energy and material stocks were reasonably well supported, although considering what Oil & Gold prices did overseas, no one got carried away, while technology tracked their overseas counterparts lower.

A quiet but (marginally) positive session played out in Oz today with the banks and miners supporting the broader index, while the Healthcare sector continues to struggle, news overnight knocking the sector again today. US CPI Inflation due for release tonight will be telling and could dictate market trends from here, just as bond yields are starting to cool.

A positive session for the ASX, its fifth in a row with the market bouncing well from the bottom of its trading range as pressure on bond yields eased underpinning broad based buying across equities, 75% of the main board finished up on the session and no sector finishing down.

Further pain was felt across the ASX today as the risk-off trade continued in the face of rising geopolitical tensions. Commodity markets took a hit, flowing through to local Materials and Energy stocks with the weakness today sending the index to an 11-month low. The recent underperformers from a sector perspective were the relative outperformers today, healthcare and Staples bucking the trend to close higher.

The ASX caught a cold from the weakness seen in the US overnight. Selling came on the back of Fed Chair Jerome Powell’s hawkish comments which sent to the US 10-year rate to 16-year highs, just a shave shy of 5%. Further tensions in the Middle East also weighed on growth assets, though that was supportive of Energy and Precious Metals, two areas of the market that largely bucked the trend today. The ASX200 fell -150pts/-2.13% during the week.

A tough day at the office for the ASX, tracking weakness in US/European markets that permeated across Asia. More tension in the Middle East is threatening higher Oil prices that would underpin persistent inflation and higher interest rates, all very logical and these concerns have pushed the ASX 200 back down to the bottom of its recent trading range.

A choppy but overall positive session at the index level, although there was a lot happening under the hood, with some hits and a few big misses to get across today.

The ASX had a positive session, although finished ~40pts below the highs after the latest RBA minutes showed another rate hike is not off the table. The list of today’s winners is an eclectic bunch with one thing in common, most have had a horrible last 12-months, perhaps some bargain hunting might be about to emerge.

A lacklustre session locally with a smorgasbord of uncertainty playing into investor minds, a -0.35% fall was okay considering the news flow. Energy and material stocks were reasonably well supported, although considering what Oil & Gold prices did overseas, no one got carried away, while technology tracked their overseas counterparts lower.

A quiet but (marginally) positive session played out in Oz today with the banks and miners supporting the broader index, while the Healthcare sector continues to struggle, news overnight knocking the sector again today. US CPI Inflation due for release tonight will be telling and could dictate market trends from here, just as bond yields are starting to cool.

A positive session for the ASX, its fifth in a row with the market bouncing well from the bottom of its trading range as pressure on bond yields eased underpinning broad based buying across equities, 75% of the main board finished up on the session and no sector finishing down.

Check your email for an email from [email protected]

Subject: Your OTP for Account Access

This email will have a code you can use as your One Time Password for instant access

Verication email sent.

Check your email for an email from [email protected]

Subject: Your OTP for Account Access

This email will have a code you can use as your One Time Password for instant access

!

Invalid One Time Password

Please check you entered the correct info, please also note there is a 10minute time limit on the One Time Passcode

To reset your password, enter your email address

A link to create a new password will be sent to the email address you have registered to your account.

Market Matters members receive daily market reports, real-time trade alerts, full access to 5 portfolios and dynamic company data.

Choose how you'd like to proceed:

We have a range of membership options to suit your needs and budget, why not join today and get unlimited access to the premium Market Matters service.