Hi Carl,

We seem to get regular questions along these lines, and by definition one day they will have some foundation – just ask Shawn, his first month on a trading desk was October 1987 – Black Monday!

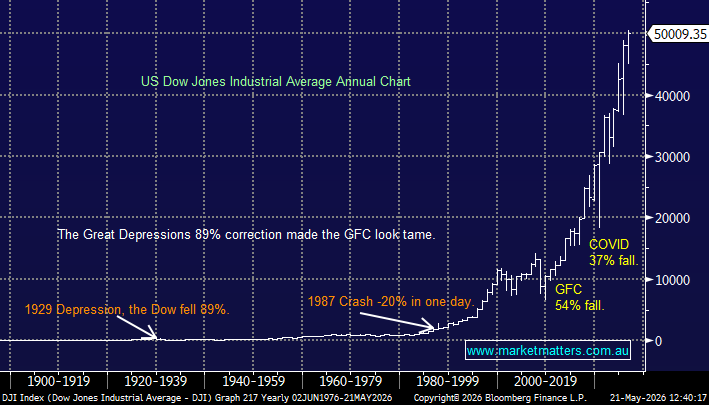

Firstly 1929: The Roaring Twenties boom showed how transformative technology can fuel both genuine economic progress and dangerous speculative excess. US equities surged nearly 500% through the decade as investors piled into the promise of radios, automobiles and electrification, amplified by rampant leverage, loose monetary policy and highly geared investment trusts. But when the Fed tightened policy and fears around the Smoot-Hawley tariffs emerged, the bubble burst violently: forced margin selling accelerated the collapse, sending the Dow down 89% from its 1929 peak to its 1932 low. The uncomfortable lesson for today’s AI-driven market is that revolutionary technology does not prevent bubbles — and once leverage and sentiment reverse together, the unwind is usually far faster and deeper than investors expect.

Now Today: The valuation backdrop is becoming increasingly difficult to ignore. With the US market trading on a PE of ~32x, the implied earnings yield is just 2.4% — hardly compelling compensation for equity risk when real Treasury yields remain elevated. Leverage levels are also relatively high in absolute terms. But unlike 1929, today’s financial system has far stronger structural shock absorbers, making a catastrophic depression-style collapse unlikely. A more plausible outcome is a painful derating akin to the post-dotcom unwind, followed by a prolonged period of weak returns as valuations normalise from extreme starting levels.

However, for Australian investors, the relative silver lining is that the ASX continues to trade at a meaningful discount to the US market, a gap that has historically mattered enormously for long-run forward returns. We haven’t soared with the AI trade and when some wind comes out of its sails, we’re unlikely to suffer accordingly.

Overall, we aren’t overly worried yet BUT if the bond market continues to deteriorate and US 30-years push much above 5.2% we will become increasingly concerned that a correction might be close at hand, but again stocks/sectors aren’t moving as one, in both directions, it’s all about portfolio structure.