Pinnacle Investment Group (PNI)

Interested in an update of your views on PNI after their recent fall?

Our Q&As are emailed in our Saturday Morning Report, find the answer to this question below.

Interested in an update of your views on PNI after their recent fall?

Hi Colin,

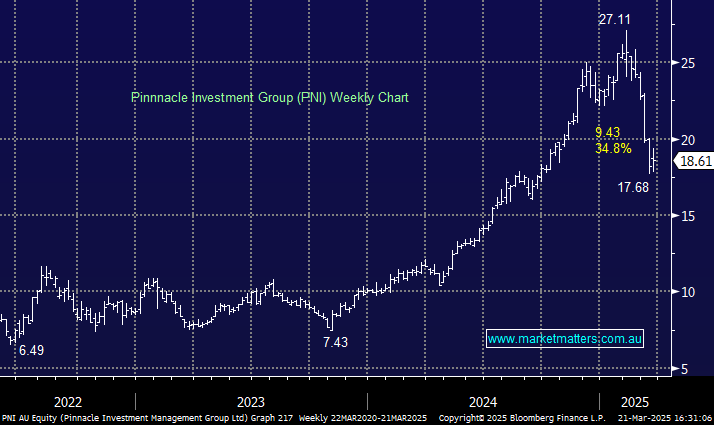

Short answer is, we think it’s a buy and have recently done just that in the Emerging Companies Portfolio. They have had a choppy week, hit by a negative article in the AFR on Metrics, which PNI owns 35% of, however, what we wrote when buying it still holds true.

PNI is a fund management group that helps independent boutique managers grow with revenue generated through fees from the management of funds and by investing in their boutique partners. PNI has evolved its business from being very focused on equity managers with earnings being vulnerable to market swings. Around COVID, PNI had $53 billion in funds under management via minority stakes in just over a dozen asset managers, including brands like Hyperion, Plato, Resolution Capital, Antipodes and Metrics. Today, that number sits at over $155 billion across 18 managers, diversified across asset classes and geographical locations, providing a significantly more robust operation.

However, PNI has still been thumped by ~35% during recent market turmoil – it remains a “High Beta” play on panic. At MM, we believe this re-rating is overdone. With the stock’s valuation finally dipping into the “cheap” area, the panic selling has not taken into account the company’s evolution over recent years, which brings with it opportunity.

The downside momentum in several crowded stocks is poor, but we believe the stock’s current entry levels will look good in the coming months/years.

Take a free trial.

No payment details required.

Forgot password? Request a One Time Password or reset your password

One Time Password

Check your email for an email from [email protected]

Subject: Your OTP for Account Access

This email will have a code you can use as your One Time Password for instant access

A link to create a new password will be sent to the email address you have registered to your account.

Hi, this is only available to members. Join today and access the latest views on the latest developments from a professional money manager.

Our Smart Phone App will give you access to much of our content and notifications. Download for free today.