Hi Debbie,

A platform business (CAR) and two software businesses (RUL & WTC) exposed to mining and logistics. CAR & WTC are large caps, and reside in our Active Growth Portfolio whereas RUL is a mid-cap sitting in our Emerging Companies Portfolio with different objectives and risk parameters:

- CAR Group (CAR) – CAR has traded ok in 2025 although its well below its November high. The company delivered a rare “miss” with its 1H FY25 numbers although it reported a 9% increase in revenue to $579 million. The stocks trading on an Est FY25 PE of 36.3x which is around average for recent years. It will need to deliver in August to be rerated back on the upside; we believe CAR’s diversified operations across multiple geographies and its focus on innovation position it for long-term growth. It’s the lowest risk of the 3.

- Wisetech Global (WTC) – This Australian logistics software is a relatively recent purchase by MM as we believe Richard White & Co are moving on from his personal issues as was demonstrated by the company’s recent purchase of E2open for $3.25bn. WTC has a long runway of growth and is trading on the cheap end of its usual valuation, we believe this will change over time. We expect WTC to outperform CAR from here.

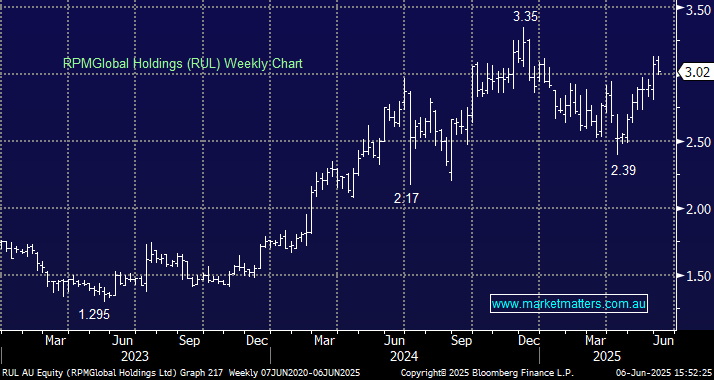

- RPMGlobal (RUL) – this company provide advanced software solutions to the global mining industry to run operations better. They reported strong 1H FY25 with revenue up 9.6% to $58.2mn and also completed the sale of its Advisory division to SLR Consulting for $63 million. We think this has a great runway from here.

We like them all: RUL biggest potential upside, biggest risk, WTC a good balance, CAR is lower risk, lower potential reward. Choose your own adventure!