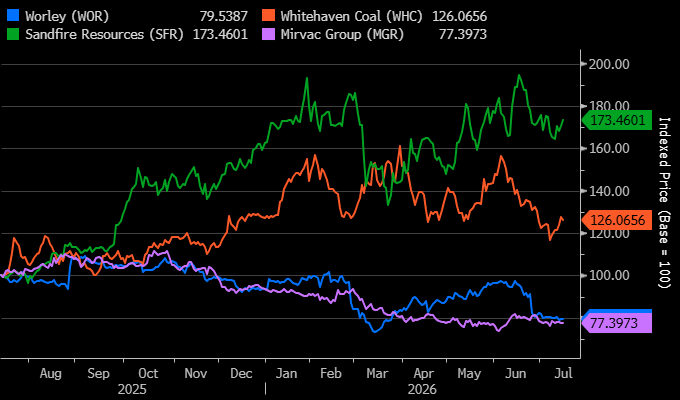

Current view on Worley (ASX: WOR), Whitehaven (ASX: WHC), Sandfire (ASX: SFR) and Mirvac (ASX: MGR)

Hi guys, would love to know your current view on a few positions in the growth portfolio - how you feel about how the buying thesis is playing out, your current levels of 'comfort' in these positions, I note they are all marked active, so would MM be buyers at these levels if you weren't in them already. Has anything changed? More conviction about some of theses? The positions are: WOR, WHC, SFR and MGR. Thanks so much for your analysis.