Hi David,

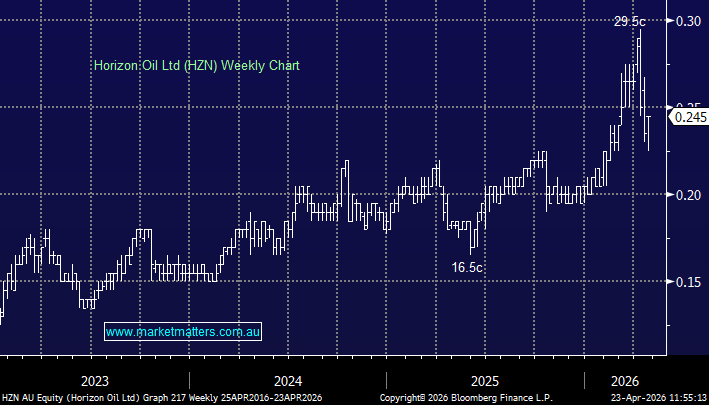

For those unfamiliar with Horizon Oil, it’s a ~$400m market cap oil producer generating ~$105m in FY25 revenue — down on all of the prior three years.

HZN is a classic small-cap oil producer — delivering real production and cash flow, with China the key earnings driver despite broader geographic exposure. The ~10% dividend yield is clearly the main attraction, but the payout ratio has exceeded earnings — a red flag. Dividends funded from capital rather than profits are not sustainable over the long term.

The key swing factor is the oil price. Recent geopolitical tensions (including Iran) have supported crude, providing a direct tailwind to earnings and helping underpin the dividend. However, this cuts both ways — if oil prices hold or rise, the yield looks more secure; if they fall, dividend sustainability quickly becomes the central risk.

As for the potential takeover of CUE: HZN & CUE have been JV partners in the Maari field (NZ) for 20+ years, along with other shared assets. Hence, this isn’t a step into the unknown — HZN is effectively buying out a partner in assets it already understands well. HZN is paying with its own shares, which has two key effects:

- Dilution: New HZN shares are issued to CUE holders, increasing shares on issue.

- Ownership uplift: HZN increases its stake in the underlying oil assets.

Despite opposition from CUE, the deal has effectively been won, the focus shifts to whether HZN reaches 90% ownership and can compulsorily acquire the remainder. Strategically we like this deal.

For investors wanting oil price leverage with an income kicker in a small-cap company— it ticks some boxes. But for MM, we think the oil price will be lower in 12 months, and the stretched payout ratio means it’s unlikely to feature in any MM portfolios.