GR Engineering Services Limited (ASX:GNG) and McMillan Shakespeare Limited (ASX:MMS)

Could I have your thoughts on MacMillan Shakespeare and GR Engineering please?

Our Q&As are emailed in our Saturday Morning Report, find the answer to this question below.

Could I have your thoughts on MacMillan Shakespeare and GR Engineering please?

Hi Julie,

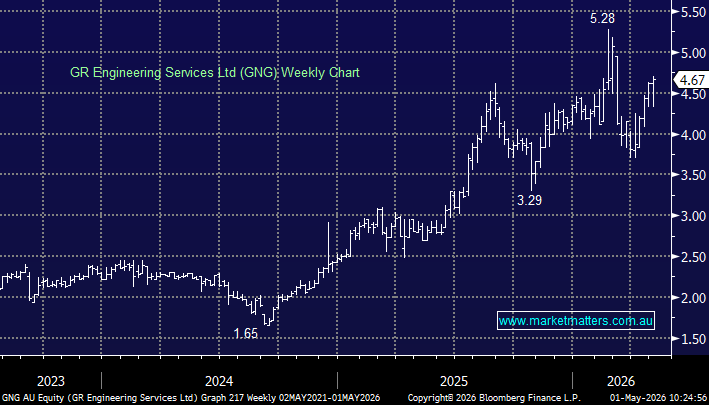

GR Engineering (GNG): This ~$800mn mining services stock would probably catch many investors attention due to its attractive 6% fully franked yield.

GNG is a specialist mining engineer and contractor that designs and builds mineral processing plants. GNG currently has ~30 studies underway, providing a solid pipeline of potential future work. While conversion is never guaranteed, E&C contractors that complete early-stage scoping and feasibility studies are often well positioned to secure the downstream EPC contracts if projects reach a positive Final Investment Decision (FID). As such, the study pipeline looks solid, albeit not a certainty.

While we like the stock, it’s important to note GNG is a highly illiquid name, where relatively small volumes can move the share price materially, making it difficult to exit in any size. Adding to the risk, earnings are inherently lumpy given its contract model, with revenue tied to one-off projects, creating a “feast or famine” cycle – for example, revenue in FY25 was $651mn, it dropped to $424mn in FY24 and is forecast to lift to $538mn in FY27.

We also note the stock is trading on the rich side of history – we would call it a cautious buy around $4.50.

McMillan Shakespeare Limited (MMS): is Australia’s largest provider of salary packaging and novated leasing services, facilitating pre-tax vehicle and benefits arrangements primarily for government and healthcare workers. The stock screens attractively at ~10.6x earnings with a yield of ~8.5%, fully franked, although this comes with an overhang, with earnings exposed to potential changes in Federal Government policy around the tax treatment of novated leasing.

MMS dropped 10% in the the session following its most recent business update and outlook, with EPS of $0.72 coming in 8.4% below the $0.79 consensus estimate. That earnings miss will keep the market on edge until further notice. We have a preference for Smart Group (SIQ) in this space, and have owned it several times in the past, though we don’t have a current position – they tend to execute better in our view.

Take a free trial.

No payment details required.

Forgot password? Request a One Time Password or reset your password

One Time Password

Check your email for an email from [email protected]

Subject: Your OTP for Account Access

This email will have a code you can use as your One Time Password for instant access

A link to create a new password will be sent to the email address you have registered to your account.

Hi, this is only available to members. Join today and access the latest views on the latest developments from a professional money manager.

Our Smart Phone App will give you access to much of our content and notifications. Download for free today.