Hi David,

We have some simple thoughts on the relatively small ~$225mn Garda Property Group, although we don’t know this stock well. Importantly, these are general observations, without taking into consideration the structure any one person invests within – i.e. General Advice Only.

GDF delivered a solid first-half result in May, with funds from operations (FFO) of $7.6m and earnings returning to positive territory after two weaker halves. Revenue continues to trend in the right direction and comfortably exceeded market expectations, highlighting the improving quality of earnings across the portfolio.

The attraction for us is the underlying asset mix. GDF remains heavily leveraged to industrial property (~83% of the portfolio), with a strong focus on southeast Queensland, a market that continues to benefit from favourable population growth, infrastructure spending and resilient tenant demand. In contrast, office exposure is limited at just 17%, reducing one of the key risks facing the broader REIT sector.

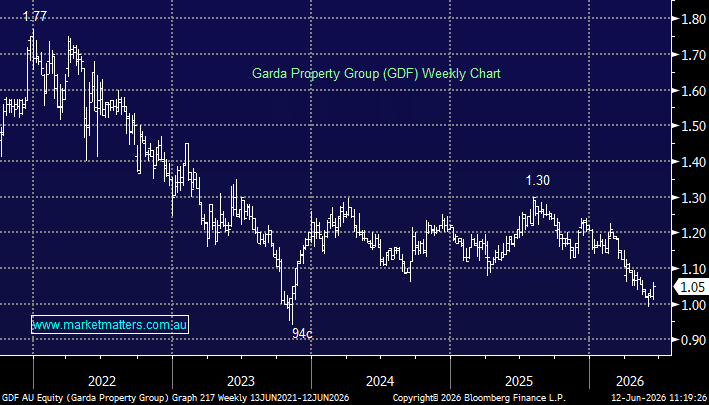

Around $1.04, GDF feels cheap trading well below its 5-year average valuation while offering an attractive yield. While small-cap REITs rarely command premium valuations, the current share price appears disconnected from the improving earnings outlook and development pipeline.

- GDF looks well positioned, albeit with the lower liquidity that comes with a smaller-cap name.