Hi David,

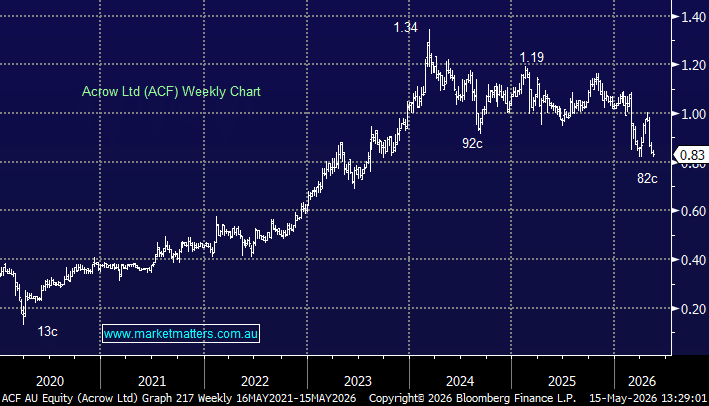

For reference Acrow (ACF) is a $260mn industrial services group that rents and supplies formwork, scaffolding and shoring equipment to construction and infrastructure projects, positioning the company as a direct beneficiary of Australia’s infrastructure pipeline, housing construction activity and the Brisbane Olympic build-out.

- Acrow screens well on the surface, its forecast to yield ~6% fully franked over the next 12-months with revenue set to increase ~30% from FY25, to $343mn in FY27.

ACF is a good business, but it has a messy balance sheet. Lots of share dilution across capital raises, rising debt and margin slippage obscure what is genuinely solid underlying revenue growth in exactly the right sector at exactly the right time.

- Its 1H26 results showed some margin slippage with the 5.68% dividend not well covered by free cash flow and interest payments not well covered by earnings.

The Olympic infrastructure tailwind hasn’t even started yet, that’s a FY27-FY30 story. The key question for August’s result is are margins stabilising and is the dividend genuinely covered? If the answer is yes, the stock looks cheap ~80c.