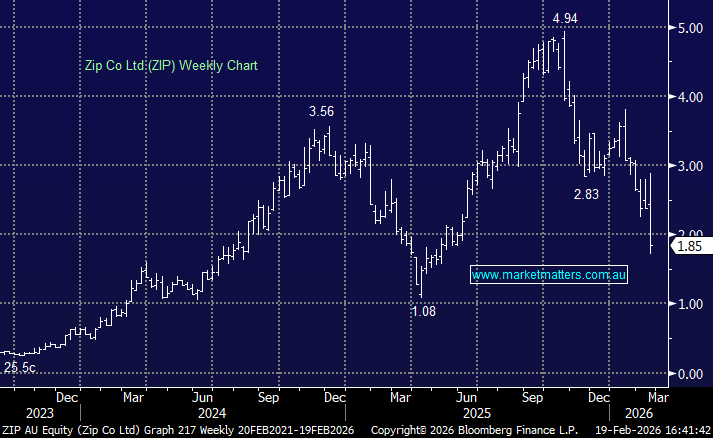

ZIP –34.4%: 1H numbers were solid, but the outlook missed the mark, guiding 2H cash earnings to be broadly flat while bad debts ticked higher. A growth business with no forecasted growth in earnings is a problem.

1H26 Highlights

- Net income: $52.4m (vs A$23.0m y/y)

- Cash EBITDA: $124.3m (+86% y/y)

- Transaction volume: $8.38bn (+34% y/y)

- Net bad debts: 1.73% of TTV (vs 1.56% y/y) + 2H cash EBITDA “broadly in line” with 1H

The market wanted acceleration, and it didn’t get it. Overlay that with an uptick in bad debts + bullish positioning, and the result is a 30+% fall. That looks overdone, but sort of understandable given 1H growth has come with deteriorating economics. The fly wheel is not operating as smoothly as it should.

MM has turned cautious on ZIP, but not a seller after a ~36% fall

Add To Hit List