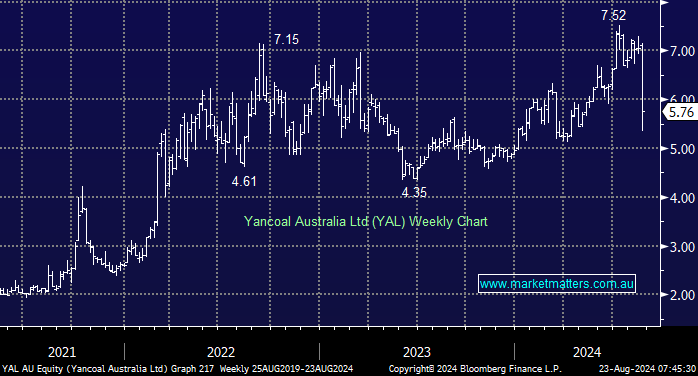

Yancoal (YAL) plunged ~15% earlier this week after withholding its dividend to build a war chest to purchase Met Coal assets, Nippon Steel beat it to the punch with Blackwater! It was a clearly unpopular decision as its yield was the main reason many investors held the coal miner. In a rare occurrence, the directors overrode the company’s constitution, which states at least 50% of net profit must be returned to shareholders – the main reason MM has avoided YAL is that it’s a proxy for a Chinese listed coal company, which will/has conducted business on its own terms – YAL now has $1.55bn on its balance sheet. Anglo American’s QLD coal mines are one of its targets.

- Further corporate action looks likely in the coal sector, as bigger businesses should reduce costs and increase their appeal to a broader pool of investors – we saw end-user Nippon Steel press the buy button yesterday.

MM is neutral towards YAL

Add To Hit List