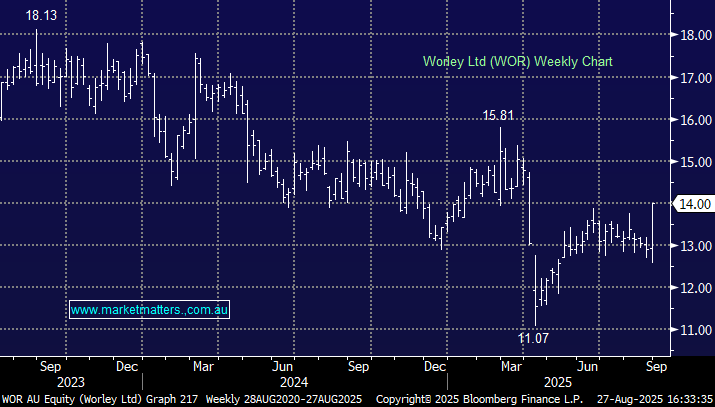

WOR +11.02%: soared today as the market looked through the FY25 numbers to the years ahead. The company is targeting higher revenue growth in FY26 than in FY25. WOR also intends to focus on costs, with AI and technology enabling it to adopt a sharper focus on overheads.

- Aggregated revenue of $12.05 billion, +3.7% YoY, but below $12.51 billion estimates.

- NPAT of $409 million, +35% YoY, came in below $421.2 million, but margins came in ahead of the company’s guidance.

- Final dividend of 25c matched expectations.

FY26 guidance looked prudent and achievable, with revenue of $13.05 billion, EPS of 0.956 and EBITDA $1.064 billion. Importantly, the guidance is much better than many feared, given recent commentary from some of Worley’s peers. Much of today’s move felt like a classic “relief rally.” Another positive was that WOR also announced it would continue its $500 million buyback on an accelerated basis.

MM remains long and bullish WOR

Add To Hit List