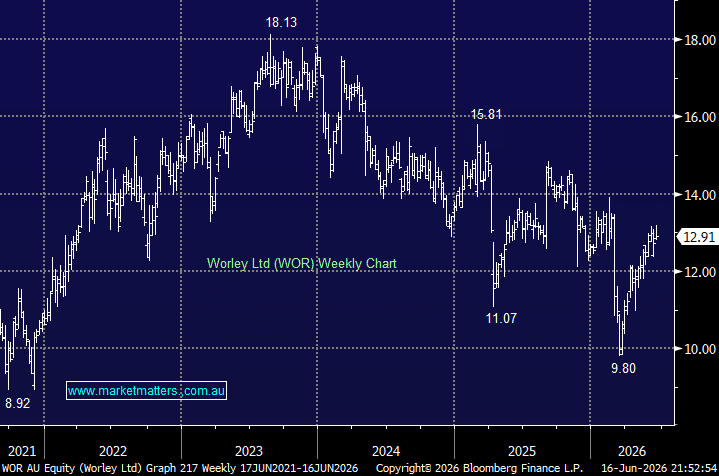

We last looked at Worley back in February after the stock fell more than 10% after its 1H result raised questions around the quality of its earnings – covered here. At the time, we held onto our position but did put it under review; today we’re glad we stuck to our guns with the stock rallying more than +30% over the last four months, in a flat, choppy market.

Worley is evolving from being a restructuring story to a backlog and execution story. While the February result disappointed the market due to $82 million of restructuring costs and flat underlying earnings growth, the company delivered new contract wins of $9.8 billion, lifting its backlog to $16.7 billion and underpinning confidence in future growth. Management has since reinforced its FY26 outlook, targeting moderate growth in both revenue and earnings (EBITA), while continuing a cost-out program expected to deliver more than $100 million in annual savings from FY27.

The company hosted an Investor Day last month, which delivered a couple of positives and, importantly, nothing that concerned MM:

- The company announced a new on-market share buyback of up to $300 million, immediately following the completion of the previous $500 million buyback program, demonstrating strong management confidence in free cash flow generation through the cycle.

- Worley’s restructuring program continues to gain traction, with $95 million of annualised cost savings already delivered and a further $25 million in progress, surpassing the company’s original $100 million target, and ahead of schedule.

- Worley is also investing heavily in the future, committing $70 million to AI and digital initiatives aimed at improving engineer productivity, reducing rework and embedding AI into project delivery.

- The company also secured a major contract with Bruce Power in Canada, reinforcing its credentials in nuclear energy, a huge growth area in our opinion.

The Investor Day delivered exactly what the market needed: a clear FY30 roadmap, accelerated cost savings, a buyback that signals balance sheet confidence, and a credible expansion into data centres and nuclear that plugs Worley directly into the two most powerful infrastructure spending themes of the coming years. The Middle East conflict has been the near-term overhang given delayed project awards and operational complexities in the region, but the backlog at $16.9 billion as of March already provides substantial earnings confidence.

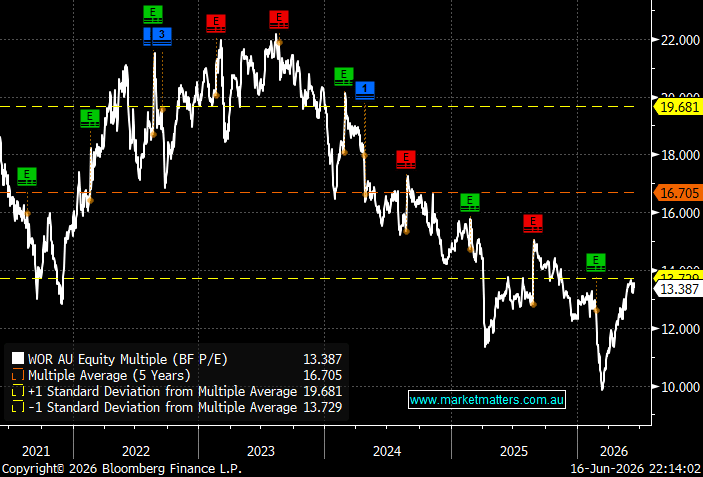

We believe that with revenue growing at a 15% CAGR since FY22 and FY26 margin guidance reaffirmed, the company appears well placed to translate its record backlog into stronger earnings. However, the market is not yet a full believer with the stock still trading 20% below its average long-term valuation.

- We believe a rerating for WOR is likely through 2026/7 as the company continues to execute successfully.

chart

Worley Ltd (WOR) historical PE – Source Bloomberg

chart

Worley Ltd (WOR) historical PE – Source Bloomberg

With the Americas generating almost 50% of WORs revenue in 1H26 the company demonstrated its ability to perform even with Middle East projects being delayed by the conflict. Moving forward we like the company’s newer focus towards data centres, nuclear and energy transition, although for now Hydrocarbons represent just over 50% of total revenue, with metals and mining at approximately 23% and infrastructure, chemicals and sustainability making up the remainder.

The numbers tell the story: Revenue for WOR has increased from $9.1bn in 2022 to an estimated $12.9bn in FY27, a lift of more than 40%, while EPS is expected to improve by even more, illustrating this is another valuation contraction story on the ASX.

- We can see WOR testing $16 in 2026, another 20-25% higher – MM holds WOR in its Active Growth Portfolio.

MM is long and bullish towards WOR around $13

Add To Hit List