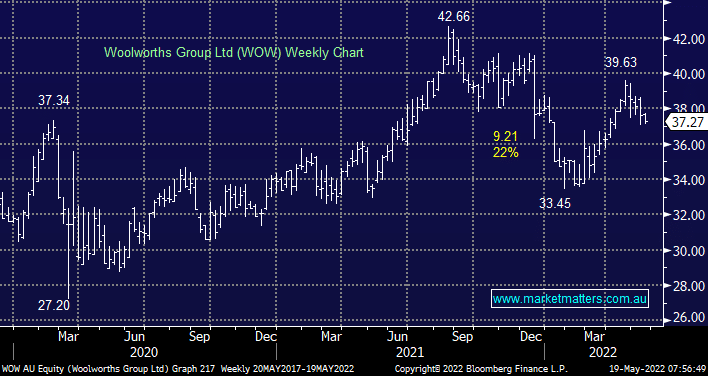

Supermarket giant WOW is in the nice position of being able to pass on price rises to the customers and often increase margins during periods of high inflation. However, it’s not all one way traffic as their rising labour costs will be adding pressure to the bottom line, I’m sure more auto checkouts are in the offing. We continue to like WOW as a defensive play aided by its conservative but sustainable fully franked 2.6% yield.

MM likes WOW around the $37 area

Add To Hit List

NB: We own WOW in our Flagship Growth Portfolio.