Before attributing this week’s neck-breaking rally entirely to Middle East optimism, investors should understand what was really happening under the surface, because a significant portion of this move had nothing to do with fundamentals and everything to do with pain. This was, in large part, a short squeeze. Goldman Sachs’s basket of the most-shorted US stocks surged more than 13%, outperforming the S&P 500 by 9% in a single week, its best showing since 2023. Traders who had built up bearish positions in financials and industrials were caught badly offside as the Iran peace narrative gathered momentum, and they had no choice but to cover. So far, around $US93 billion in short positions has been unwound across US stocks this month, pushing up both the S&P 500 and Russell 3000 more than 9%.

Institutional investors and algorithmic funds had compounded the problem by slashing equity exposure to multi-month lows ahead of the bounce. When the catalyst arrived, the forced buying from short covering collided with genuine re-engagement from underweight funds, and the result was a move that felt far larger than the underlying news arguably warranted. The geopolitical risks haven’t been resolved. Oil prices remain elevated and inflation implications are still unknown. However, the strength has not been universal across the market: An equal-weighted version of the S&P 500 Index, which makes no distinction between a behemoth like Microsoft Corp. and a relative minnow like News Corp., is still 0.6% below its record, and the old-economy Dow Jones Industrial Average sits 1.4% away from its February peak.

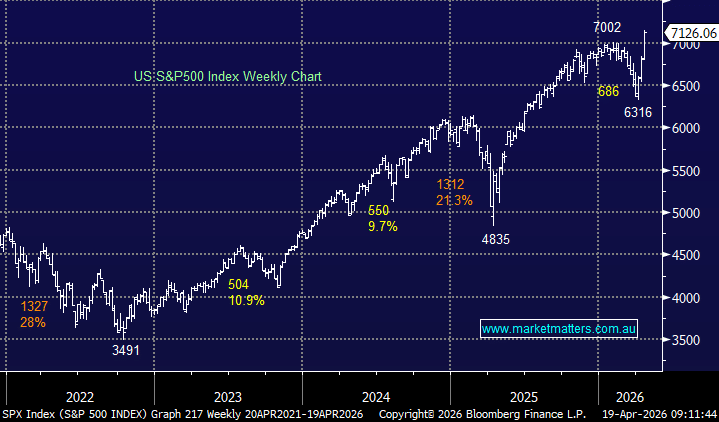

- We can see the S&P 500 taking a rest before punching higher, but we are far more “buyers of dips” than “sellers of strength.’

MM is bullish towards the S&P 500 around 7100

Add To Hit List