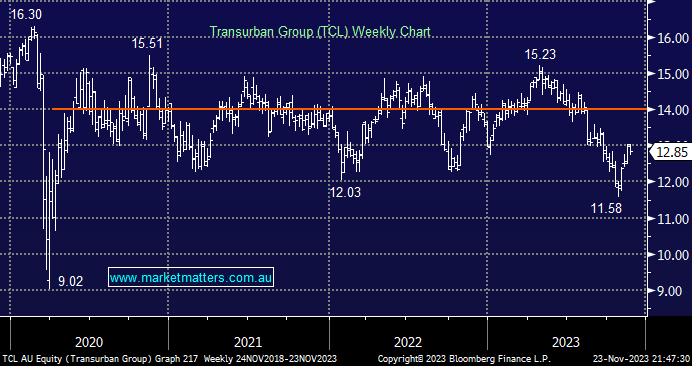

We discussed TCL at length earlier in the month in a Portfolio Positioning report, the conclusion being that TCL will look appealing when bond yields do turn meaningfully lower. While it’s not our first pick at this stage, this may change depending on respective prices at the time.

- We like TCL as a quality defensive play moving into 2024, while their estimated ~5% yield isn’t as compelling as some alternatives, it is now very sustainable with a tweak to their payout policy in recent years.

MM is cautiously bullish toward TCL

Add To Hit List