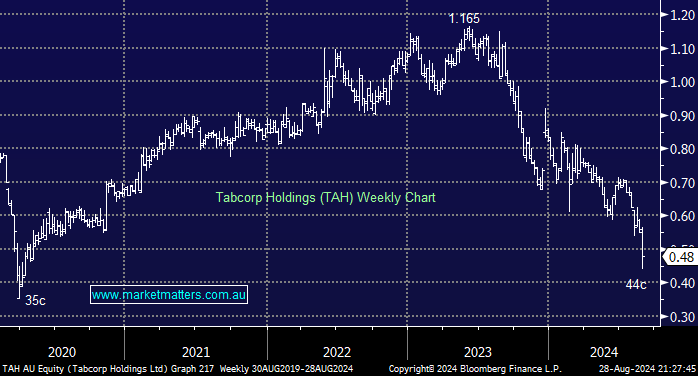

TAH was whacked 15% on Wednesday after delivering an FY24 earnings miss and weak guidance that it expects soft market conditions to continue. There were some positives, such as the company securing a new 20-year Victorian Wagering and Betting Licence and progress in upgrading its retail venues. Still, these were outweighed by the company’s struggles in the digital space, with revenue down 2.2% for the year. TAH still looks and feels like an old-fashioned “dinosaur-like” business falling ever further behind in the growth area of its marketplace.

- Group Revenue was down -3.9% yoy to $2.34bn, and EBITDA fell -18.7% to $317.7mn.

- Net profit before significant items was $28mn, down -67% from the previous year.

- Declared a dividend of 0.3 cents per share, unfranked, a 43.5% decrease from FY23.

The new Tabcorp chief executive has acknowledged that the business will not meet cost-cutting targets and optimistic aspirations to take a 30% share of the digital wagering market by next year. Mr McLachlan has followed in the footsteps of many new CEOs by clearing the decks and writing down assets wherever possible. However, we can see nothing in this result that suggests it is time to catch the falling knife; the company needs a huge freshen-up to lure the younger generation of online punters, but it’s an incredibly competitive space.

MM sees no reason to own TAH

Add To Hit List