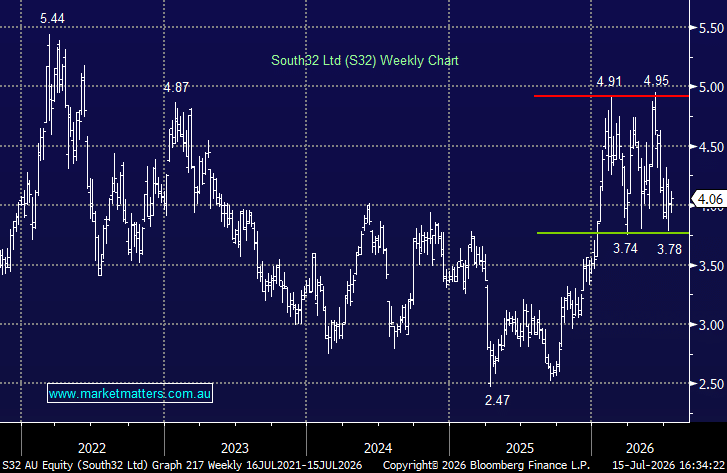

S32 has transformed itself in recent weeks after selling off its aluminium value chain, including Worsley Alumina, Hillside Aluminium and its Brazilian bauxite and alumina assets, to Alcoa for an implied US$5.6bn. The package comprises US$3.1bn in cash, around US$1bn in Alcoa shares, assumed liabilities and contingent payments linked to future aluminium prices. The assets accounted for around 60% of group earnings, making this a transformational portfolio reshaping.

Post-transaction, around 85% of South32’s pro forma earnings (EBITDA) will come from base metals, primarily copper, zinc, lead and silver, with the company expected to hold US$3.8bn of net cash and benefit from Alcoa assuming around US$1.2bn of rehabilitation liabilities. Management also expects US$125m of annual overhead savings by FY29. We like this simpler, copper-focused portfolio as a potential re-rating catalyst, although we are conscious of our large copper exposure moving into the 2H – good job we’re bullish!

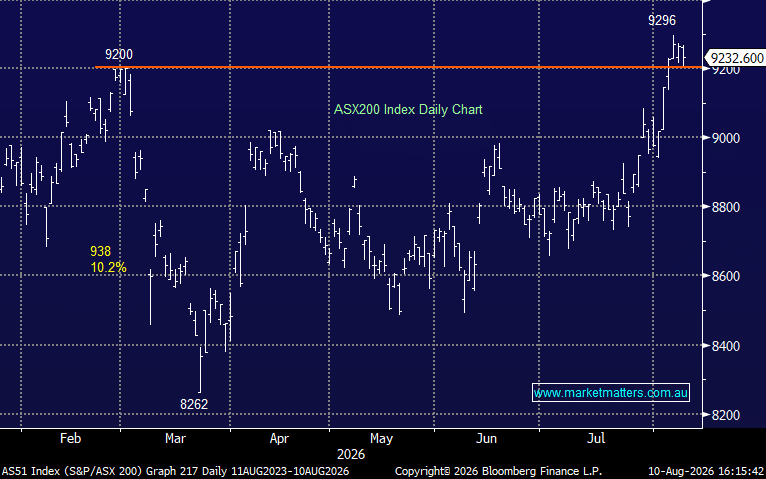

- We like the risk/reward towards S32 around $4, targeting a retest of $5, or ~25% higher – MM holds S32 in the Growth Portfolio.

MM is long and bullish towards S32 around $4

Add To Hit List