MM bought S32 last month for our Active Growth Portfolio when it wasn’t on our Hitlist; hence this morning we’ve discussed the stock and our reasoning to gain exposure to the miner following its recent pullback.

Firstly, our outlook on S32’s current primary sources of revenue:

- Aluminium: We remain constructive on aluminium, with production costs and a favourable copper-to-aluminium substitution trend likely to offset the impact of rising supply, particularly from Indonesia, as the market rebalances through 2027–28.

- Alumina: We’re more cautious on alumina, where subdued demand and ample refining capacity has weighed on near-term pricing.

Aluminium is quietly emerging as an electrification winner, with years of underinvestment colliding with accelerating demand from power grids, EVs, aerospace and AI data centres, while new supply remains constrained by high energy costs and environmental hurdles. While the above comments don’t sound as bullish as our outlook towards Cu, it’s the very reason why we waited for a ~20% pullback in the miner before buying last month.

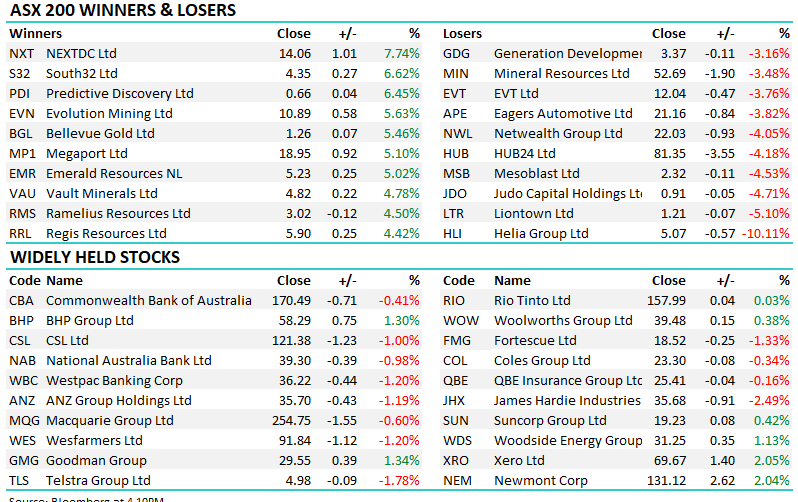

Importantly, as the chart below illustrates, the current weakness across the miners, courtesy of a strong US dollar, has led to an almost disconnect between S32 and the Aluminium price, producing a great risk/reward opportunity into FY27.

South32’s latest trading update reinforced the strength of its diversified global portfolio, with FY26 production guidance reaffirmed across most operations despite weather disruptions and the planned closure of its Mozal Aluminium smelter. Management continues to prioritise growth in future-facing commodities through the Hermosa project in Arizona, while stronger aluminium prices, resilient production at Sierra Gorda and a robust balance sheet leave the company well positioned to benefit from the long-term electrification and energy transition themes.

NB Despite its recent capex blowout, Hermosa will transform South32 into a larger producer of future-facing metals, with the first stage delivering zinc, lead and silver, followed by battery-grade manganese, while the broader district also offers significant long-term copper upside.

- While revenue is forecast to be flat ~US$6.75bn in FY26 and FY27, EPS is encouragingly forecast to grow by almost 40%.

There’s a comparison with BHP, the very miner that spun out S32 back in 2015: South32 is evolving its commodities mix using cash flow from aluminium as a funding source, just as BHP did with iron ore.

- We like the risk/reward towards S32 below $4 and may “top up” our position in FY27.

MM is long and bullish towards S32

Add To Hit List