Global trends matter for local stocks, helping shape how we think about opportunities closer to home. Last week, Booking Holdings (owner of Booking.com, Priceline and OpenTable) reported a strong set of numbers – earnings up 32%, bookings across their platforms up 13% YoY, and profits beating consensus by 10% thanks to better margins. On the conference call, management flagged steady global travel demand into the September quarter, despite ongoing macro and geopolitical uncertainty.

That’s a positive read‑through for SiteMinder (SDR), which provides cloud software to help 40,000+ hotels manage and grow bookings. SDR’s revenue is heavily linked to room night demand, particularly among smaller and independent operators. Back in May, a string of local travel companies flagged softer conditions, while international players were more upbeat – albeit still cautious on the US. Booking again noted last week that US growth is lagging, but it’s being more than offset by strength elsewhere, particularly in Asia and Europe. The Americas contribute ~30% of SDR’s revenue, so weakness there matters – but it’s also a known known, creating potential upside when US consumer confidence rebounds.

Confidence is starting to build elsewhere, even as Jerome Powell and the Fed hold off cutting interest rates. Lower rates are only part of the story, but they will help travel names like SDR.

- Looking longer term, Citi forecasts SDR’s revenue to grow ~80% from $188m (FY24) to $351m (FY27), driving a 250% uplift in earnings. SDR is still unprofitable (FY25 loss tipped at ~$12m) but it’s scaling well – a path similar to Xero (XRO) in its earlier days – and at scale, the earnings power could be significant.

We increased SDR to a 6% weighting in the Emerging Companies Portfolio in May (~$4.40) given our conviction. FY25 results drop on 27 August.

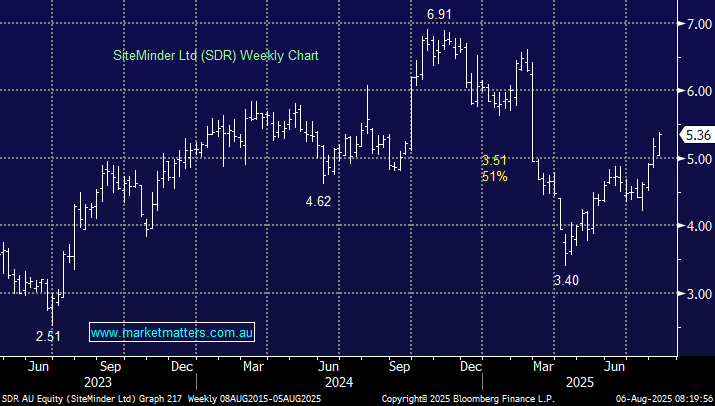

MM remains long & bullish SDR ~$5.30

Add To Hit List