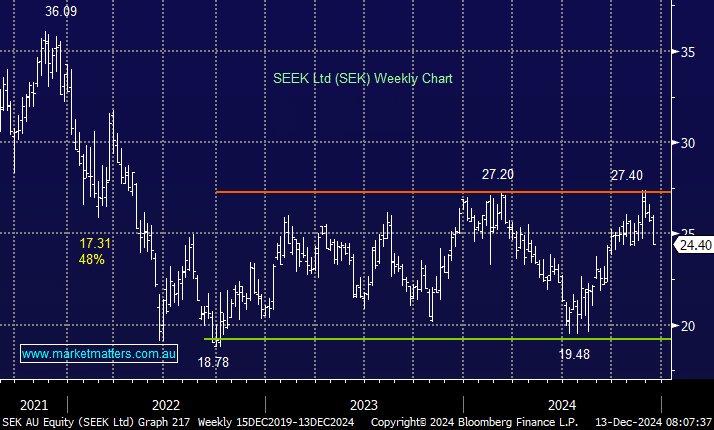

SEK has struggled to keep pace with CAR and REA post-COVID, and the August FY24 results did not help; they delivered lower-than-expected earnings for FY24 and a decent downgrade to FY25 guidance. We regard SEK as a quality business, but it hasn’t figured on MM’s Hitlist due to lacklustre returns from overseas expansion and the clouded economic picture for the local economy.

- We see no reason to fight the last few years’ sideways trend in SEK, especially with the stock towards the top end of the range.

MM is neutral towards SEK

Add To Hit List