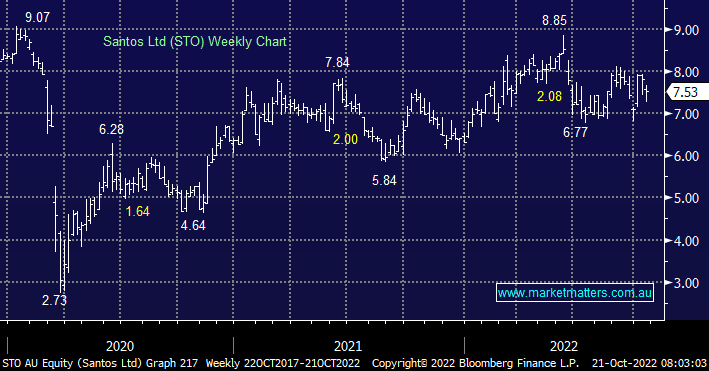

STO recently sold down its 5% equity in PNG LNG, strategically the sell-down partly mitigates STO’s country risk exposure to PNG but also accelerates deleveraging to support further capital management, helping to drive a re-rate and alleviate some commodity price volatility. With a breakeven around $US35/barrel we see significant balance sheet capacity for major on-market buybacks, something in the order of $500m looks realistic. STO is trading slightly cheaper than WDS on 5.7x 2022 earnings although its yield is closer to 5%.

- We prefer WDS over STO although some would argue the latter is cheaper but it could remain so for years.

MM is neutral to slightly bullish STO

Add To Hit List