Yesterday morning it emerged that Regal was in talks with Platinum Asset Management (PTM) to acquire the well-known, but recently out of favour fund manager for around $660m. If successful, RPL would pick up $12.2bn of Funds Under Management (FUM), adding to RPL’s current $16bn pile. The deal makes sense on several levels, and after failing to ‘win’ Perpetual back in November of 2022, when RPL bid $33/sh (PPT closed yesterday at $18.57), they are back in the hunt for a big deal.

RPL has made several acquisitions since, but none as big as Perpetual would have been, or Platinum could be. For context, Regal is worth ~$1.1bn with $16.5bn or FUM, while PPT is worth $660m with $12.2bn of FUM, or put another way, PTM is worth ~60% of RPL with ~74% of the FUM – but it gets better for RPL. PTM has around $300m cash & investments on the balance sheet plus ~$70m of franking credits, meaning RPL could be picking up the FUM for around $300m.

Performance at Platinum has been the issue, which has led to outflows since listing on the ASX in 2007. Those with a good memory might recall the phenomenal day 1 performance for PTM, with the stock up 76% from its $5 issue price to close the day at $8.80. At the time they had ~$22bn of FUM and were flying. At yesterday’s close of $1.115, the stock has declined by ~80% from the IPO price, while FUM has nearly halved. Over the past 10 years, PTM’s flagship strategy, the Platinum International Share Fund has returned 7.6% pa versus its benchmark of 12.3% pa. With such significant underperformance over an extended period, the outflows are understandable.

The playbook for RPL is simple. Use more highly valued scrip + some of the cash balance of the target to buy a significant amount of FUM and improve performance. PTM has a good distribution network which RPL could utilise for the distribution of its own more diverse collection of strategies, that span local and global equities, short and long strategies, specialist products such as water, agriculture and resources, and private credit.

For PTM shareholders, RPL is proposing a 24c fully franked dividend which equates to ~34c paid from PTM cash and franking, plus 0.274 RPL shares, with the deal worth $1.217 based on yesterday’s close. Presumably, RPL has Kerr Neilson on board, who still owns over 21% of PTM.

- While it’s only early days, we would not be surprised if the bid amount is increased, believing it still makes sense for RPL at a price up to 10% higher.

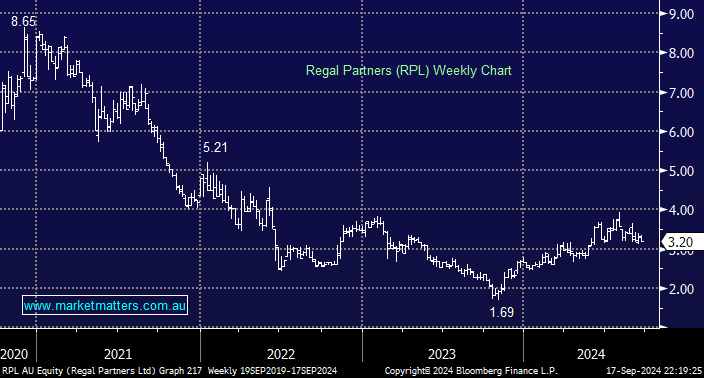

MM remains long & bullish RPL

Add To Hit List