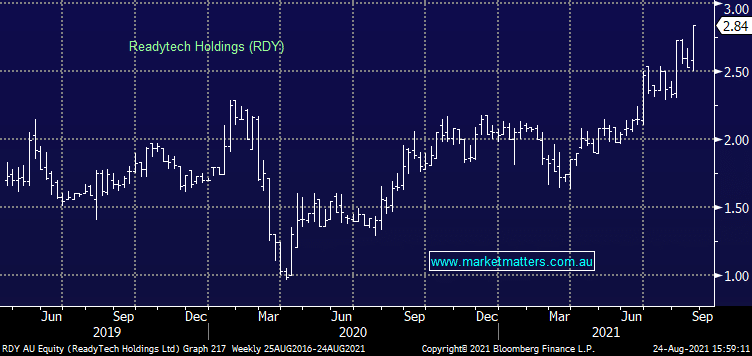

FY21 Result: The impressive education technology business posted a solid FY21 result today (~1% above Shaw’s expectations) however they outlined a path of strong organic revenue growth over the coming 5 years which speaks to increasing confidence from management and line of sight for the business. Shaw’s analyst Jules Cooper had this to say on the result… FY22 guidance implies an acceleration in organic growth to 18% vs 13% achieved in FY21 on a like-for-like basis. In addition, RDY have provided a new FY26 organic revenue target of +$125m, which is approx +20% ahead of our prior forecasts and demonstrates management’s growing confidence in the business and outlook. We have upgraded our FY22-24 revenue forecasts by 5-14% and EBITDA by 3-13%. We upgrade our PT to $3.60 (was $3.00) and believe the re-rate can continue.

MM is bullish RDY

Add To Hit List