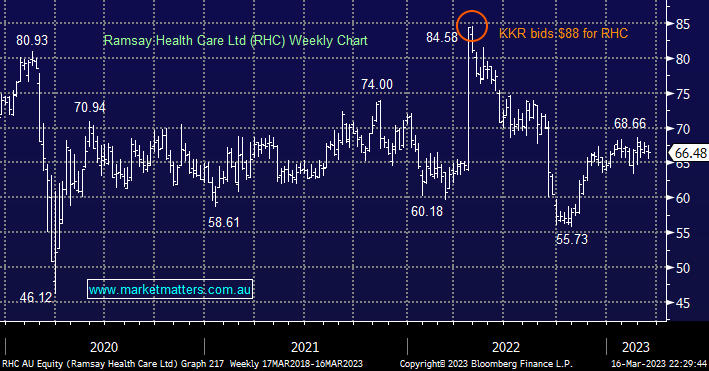

RHC has experienced a tough few years firstly with COVID putting elective surgeries on ice, not good news for private hospitals. Then last year KKR walked away from a $88 bid, while we understand why they walked with the messy ownership in France it does illustrate that the investment manager values the stock significantly higher i.e. if it was prepared to pay $88 it saw a value closer to $100 after it weaved its magic.

- We have flagged our positive outlook on RHC over recent months as the economy evolves post-COVID, we can see a 10-20% upside.

- RHC is our likely vehicle of choice if we move overweight the Healthcare Sector.

MM likes RHC under $65, or 2-3% lower

Add To Hit List