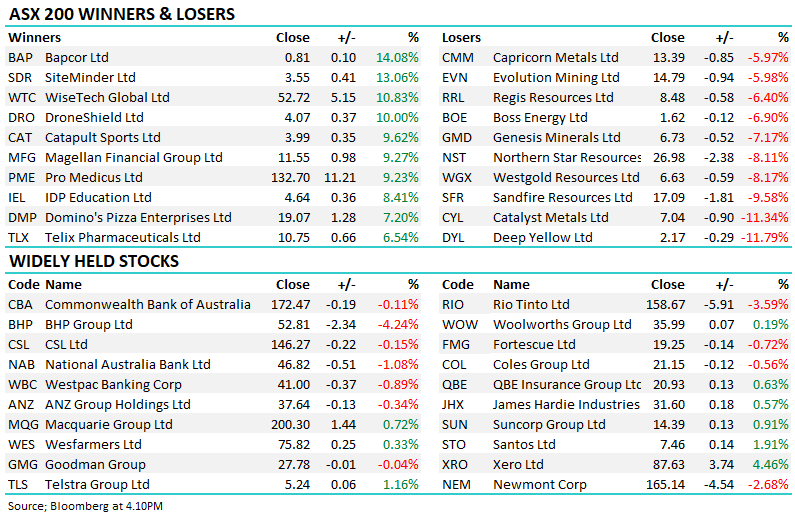

Arguably, PME personifies the high growth unwind across the ASX, as this software provider for medical practices has plunged almost 35%. The severity of the decline can be attributed to a few things: it was a highly outperforming growth stock that had momentum traders all over its registry, it is relatively illiquid, moving a few dollars in the blink of an eye, and it needs ongoing fresh contract wins to justify its lofty valuation. With the uncertainty that Trump tariffs have created, corporate America has “shut up shop” until the muddy waters clear, making it harder for PME to maintain its impressive track record of contract wins; hence, we are classifying it as more suitable for a trade, but it is a business we like.

- We like PME for at least a bounce back up towards $250, or 20-25% higher.

MM likes PME as a trade

Add To Hit List