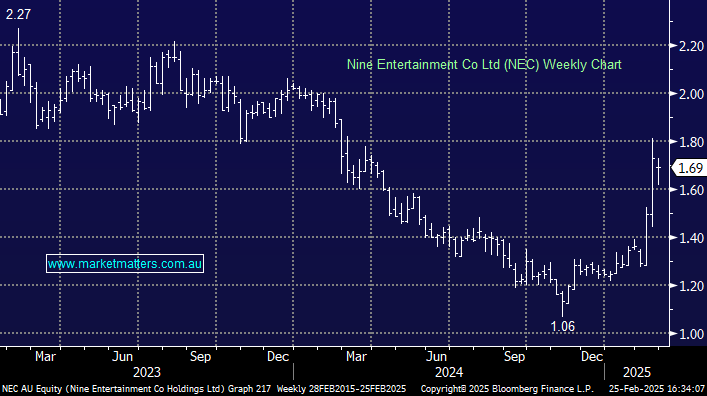

NEC +3.68%: Reported a softer operational result year-on-year, in-line on revenue but impressing on guidance around cost-control and efficiencies moving forward.

- Revenue $1.4bn, +1.6% yoy vs. $1.42bn consensus

- Net profit $96mn, -15% yoy

- $50m targeted cost-efficiencies for FY25, $10m-$20m to be realised in FY25, with long-term efficiencies through FY27 forecasted at ~$100m.

Nine anticipates further restructuring into 2H25 and FY26, with ongoing cost efficiencies supporting profitability. Broadcasting revenue is forecasted mid-to-high single-digit growth though ad revenue is expected to decline to high single digit growth, so a solid outlook from a sales perspective.

Management reiterated their stance on the sale of Domain i.e will consider CoStar’s proposal with a focus on best interests to shareholders… we’ve heard that one before and we know given its strategic value, it will not be given up easily.

MM remains long and bullish NEC

Add To Hit List