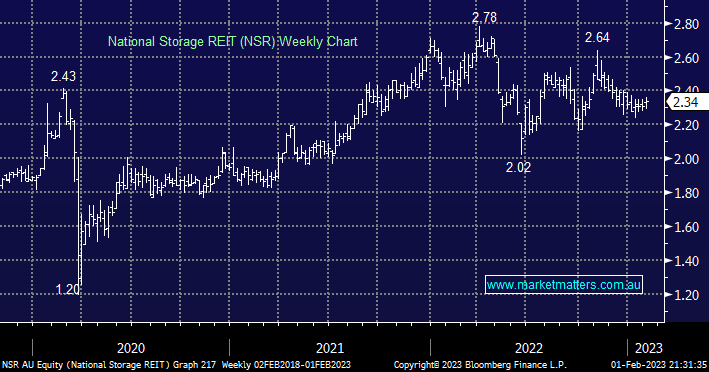

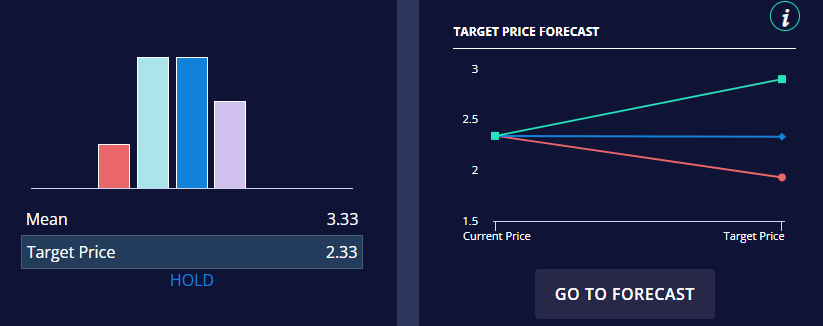

Self-storage business NSR is forecast to yield 4.9% unfranked over the next 12 months, a supportive reason to like NSR but certainly not a standalone reason to buy. One positive for the business is its ability to re-price rents in today’s inflationary environment due to shorter-duration contracts although like many companies it’s still likely to see a dip in earnings if we do experience a deep recession, we believe the stock’s recent ~10% correction is starting to fully price in a local cash rate ~4% but most brokers don’t agree with us i.e. 1 strong sell, 3 sells, 3 neutral and only 2 buys with a consensus price target of $2.33 which can all be viewed here.

- We rarely like buying stocks that cannot rally in a strong sector and NSR is no different hence at this stage we are only considering the stock 6-8% lower.

MM likes NSR under $2.20

Add To Hit List