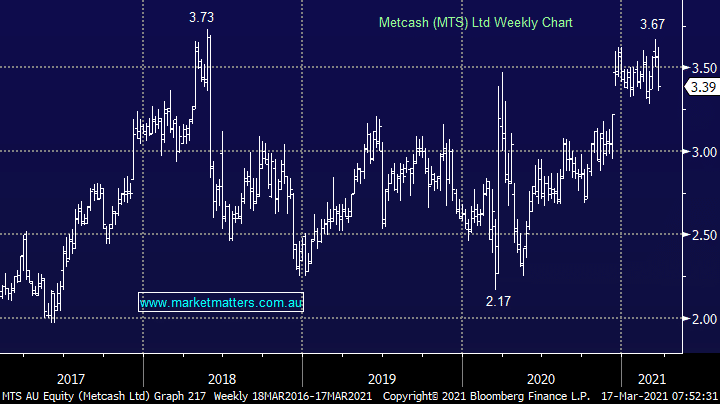

Portfolio holding Metcash (MTS) held an investor day yesterday and also delivered a trading update and moved their dividend payout guidance up from 60% to 70%. MTS trade on an Est P/E of 13x and they are forecast to yield 4.57% fully franked over the coming 12 months. Like the other Supermarkets / Hardware operators, MTS have been COVID beneficiaries and the sales momentum has continued in the first 4 months of the 2H. I thought yesterdays update was a strong and set our a credible strategy for MTS over the coming 5 years. The stock was initially higher on the news however was sold off throughout the session.

To MM, it was guidance around higher costs to drive the revitalized strategy that got the sellers out which is a valid concern. I came away from yesterdays update thinking they have a lot of work to do to tap into the big opportunity online, plus of course streamlining the wholesale / distribution services underpinning their independent operators.

Metcash has been the poor cousin of the majors for as long as I can remember, however they now have a very strong balance sheet, a growing business that is improving incrementally in all areas, and they remain too cheap in MM’s view.

That balance sheet capacity should also bring in further thoughts of capital management initiatives at their full year results.

MM remains bullish MTS despite higher cost guidance

Add To Hit List