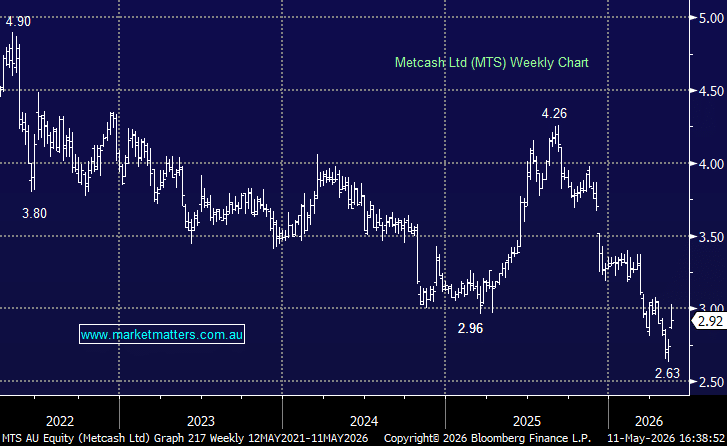

MTS +6.57%: has been a frustrating holding in the Income Portfolio recently, with the stock weak into today’s update as investors worried about softer hardware conditions, margin pressure, freight costs and broader consumer weakness. Today’s update should go some way to allaying those near-term concerns, with FY26 guidance broadly in line at the group level, but importantly, better than feared across the key Food and Liquor divisions.

Key takeaways:

- FY26 revenue expected at $19.6bn, up 0.7% on the prior year, or +3.8% excluding tobacco.

- Underlying NPAT expected between $268m and $270m, broadly in line with consensus at ~$270m.

- Food EBIT guidance of $259m-$262m, modestly ahead of expectations, with the division continuing to show resilience.

- Liquor EBIT guidance of $98m-$101m, around 4.5% ahead of consensus, helped by margin recovery in the second half.

- Hardware and Tools sales momentum improved in the second half.

- No material FY26 earnings impact from higher freight or product costs has been seen to date, despite broader supply chain concerns.

The market took the update positively because the divisional detail was better than feared, particularly in the core defensive parts of the business. Food and Liquor remain the backbone of the Metcash investment case, providing a relatively defensive earnings base through the company’s role as the wholesale supplier to independent retailers across IGA, Cellarbrations, The Bottle-O and other banners. These divisions are not immune to cost pressure or changing consumer behaviour, but today’s numbers suggest they are holding up reasonably well.

Hardware has clearly been the problem area, with the cycle turning against the business as housing activity and discretionary renovation spend softened. However, the update also pointed to improved sales momentum in Hardware and Tools during the second half, alongside structural cost actions.

The other positive was the cost-out program. Metcash now expects at least $25m of annualised savings in FY27, with around $6m of restructuring costs and payback inside 12 months.

While the Middle East conflict remains in focus, Metcash said there has been no material impact on FY26 earnings from higher freight or product costs to date, and no supply shortages. The company has increased inventory levels as a precaution, which may weigh on working capital temporarily, but it is a pragmatic move given the current uncertainty.

- Overall, today’s update was better in the areas that matter most. Food and Liquor remain resilient, Hardware looks to be stabilising, and cost savings should support FY27 earnings.

MM remains long & bullish MTS (for Income)

Add To Hit List