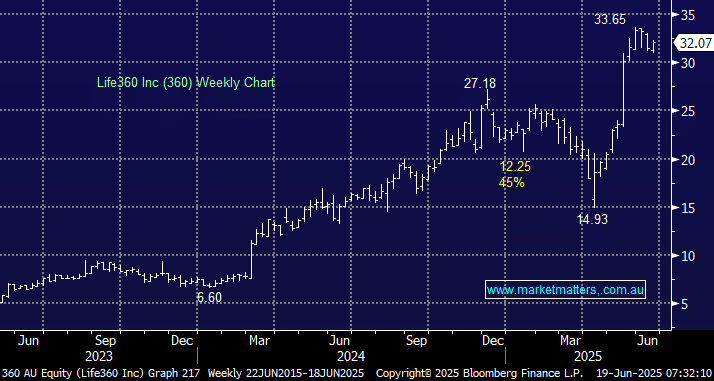

We have covered 360 a few times in 2025 and it’s a company we’ve liked and ultimately been too slow to buy. The shares surged higher in April after the tracking App delivered better than expected 1Q results, with revenue up over 30% and monthly active users up 26%, the 10th consecutive quarter of positive adjusted earnings. Importantly its improving operationally with a 23% increase in expenses vs the 32% uplift in revenue, plus a pop in growth is around the corner with its pet tracking app due in Q4 – never underestimate how much people love their fur babies, it’s estimated to already be well over a half a trillion dollar industry today, with forecasts expecting that to nearly double by the mid-2030s.

We like 360 and they have a huge runway to monetise their user base – we should have owned the stock (kicking ourselves!) however, it’s very stretched after a great run, and we’d like to get more insight into both the pet roll-out and how advertising will drive future earnings.

MM is neutral/cautiously bullish 360

Add To Hit List