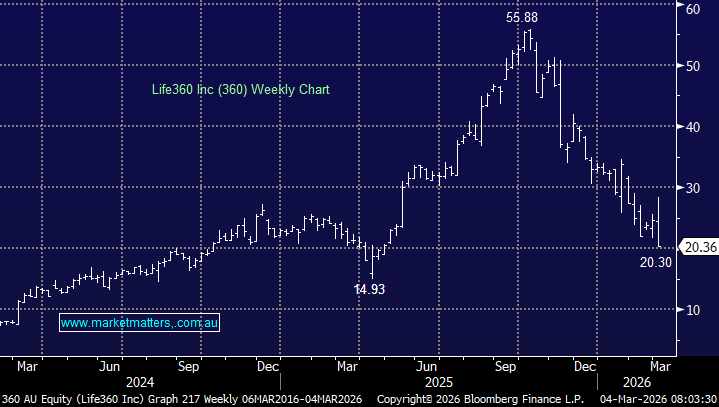

The global family safety platform Life360 reported 4Q and FY25 results yesterday, and after trading up ~15% early, the stock closed down ~17% – a staggering 32% turnaround on the day! The result itself was strong.

FY25 Highlights

- Profit: $US150.8 (vs $US8.5m prior year) – although there was a one-off tax benefit here ($118m). Underlying profit was $US32.5m, its first annual profit.

- Revenue: grew 32% to $US489m – ahead of consensus ($486.8m)

- Monthly Active Users were 95.8m

360 has two versions. A free version and a paid subscription. Subscription revenue, both US and international, rose solidly. Hardware revenue declined, which was expected, and management is now guiding hardware to fall to $40–50m in 2026 as the mix shifts further toward higher-margin subscription and platform revenue. When talking hardware, we’re primarily talking about Tile, which they acquired in 2021 – the bluetooth-enabled tracking devices used to locate keys, wallets, bags etc

- Looking forward, they guided to FY26 revenue of $US640m–$US680m (31–39% YoY growth), and MAU growth of +20% to ~115m users. These numbers were the reason why the stock traded higher initially, but the market focused elsewhere. Two concerns drove the sell-off.

First, management warned that user growth would be slower this quarter, with stronger momentum expected in the second half as new features and international campaigns roll out. Markets tend to punish even temporary slowdowns in high-growth names, particularly when sentiment is already fragile.

Second, tariff uncertainty has complicated their hardware strategy. Plans to move Tile manufacturing out of China have been paused pending clarity on US trade policy. That adds short-term uncertainty around hardware margins and supply chains, even though hardware is becoming a smaller part of the overall revenue mix.

Overlaying all of this is the broader AI narrative. There is concern that AI-driven location or coordination tools could erode Life360’s model. Management pushed back strongly on this, arguing that their proprietary location, behavioural and real-world safety data cannot be replicated by generic AI tools. We think their point is reasonable, given 360’s value proposition is embedded in physical-world services like crash detection and roadside assistance, not just code.

On the face of it, the business continues to execute well; Strong double-digit subscription growth, expanding international contribution, operating leverage as scale builds and a clear pivot away from lower-margin hardware. Revenue growth of 30% in FY26 was a solid guide, even though it was a shade below consensus.

Timing was an obvious issue, with growth in users expected to be back-end loaded this year. Advertising is also now a driver of earnings (for the free version), and that has cyclicality to it. They’re also spending more on growth in the 1H, which will have a negative influence on margins. But all that said, the business is stronger than it was 12–18 months ago – the mix is improving, profitability is coming through, and management continues to invest (sensibly, we think) for growth over the medium term.

We’re (uncomfortable) holders in the Emerging Companies Portfolio given the recent weakness in the share price, but we still believe the medium-term trajectory, particularly as subscription revenue builds, remains attractive.

MM is cautiously bullish 360 ~$20

Add To Hit List