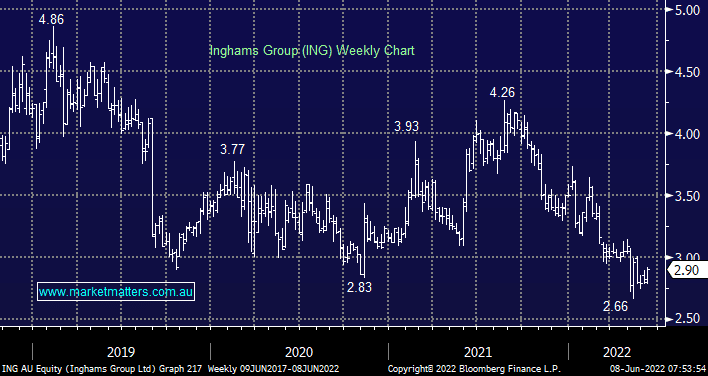

Poultry supplier ING has been hammered over the last few months, a raft of issues ranging from fuel and feed costs plus labour shortages have hurt both the cost and scale of production, although the latter has at least improved as we move on from COVID. MM continues to like the relative stability of the business if these issues can be overcome while chicken being a cheaper protein selection to say steak should limit the impact of less $$ sitting in the pockets of consumers.

The stock pays a very healthy fully franked dividend which is likely to be supportive in today’s uncertain environment and in our opinion the current operational headwinds appear likely to have peaked, hence the stock looks good value under $3.

MM likes ING under $3

Add To Hit List