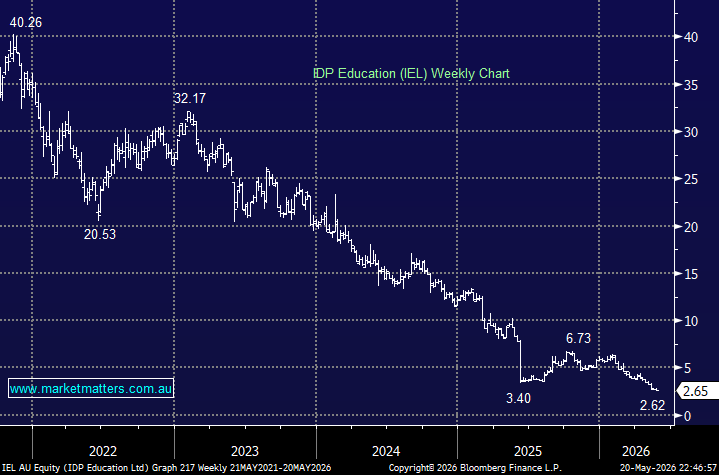

IDP Education operates a global international student placement and English-language testing business, generating revenue by helping students enrol in universities abroad and administering IELTS exams. The company earns fees from universities for placing students, commissions from counselling and placement services, and high-margin testing revenue through IELTS, which remains one of the world’s leading English proficiency tests for migration and education purposes. We last looked at IEL in late 2025 here, as the company was being weighed down by government policy, never a great corporate position. Another previous market favourite, although in this case the stock has crashed well over 90%.

The company’s revenue has oscillated in the $850mn-$1bn region over the last 5 years, with IDP becoming one of the most policy-sensitive stocks on the ASX, with the share price now driven far more by government visa settings than management execution or underlying business quality. The key question is no longer whether international education demand exists; it does over the long term, but when major markets such as Australia, Canada and the UK begin easing restrictions on student inflows. At current levels, the market is pricing in a prolonged and uncertain recovery. For long-term investors, that may ultimately prove an attractive entry point into a high-quality franchise tied to a powerful structural trend, but patience will be required, given there is little visibility on when the policy backdrop improves.

Australian universities have built business models that are heavily reliant on international student fees, leaving the sector almost as exposed to migration policy as IDP itself. That dependency is arguably IDP’s strongest long-term support; governments can tighten settings temporarily, but sustaining severe restrictions indefinitely would risk damaging university funding, research capability and the broader knowledge economy. A higher student cap for 2026 may be the first sign that policy is beginning to shift back toward balance. Importantly, the business remains profitable and cash generative, but the market no longer views growth as predictable, while global governments remain focused on reducing migration and student inflows. A ~3.8% yield, part franked, will help patient investors.

- We can see IDP doubling, as it did in 2025, but this is a volatile policy-driven stock that comes with plenty of risk.

MM is cautiously bullish towards IEL around $2.50

Add To Hit List