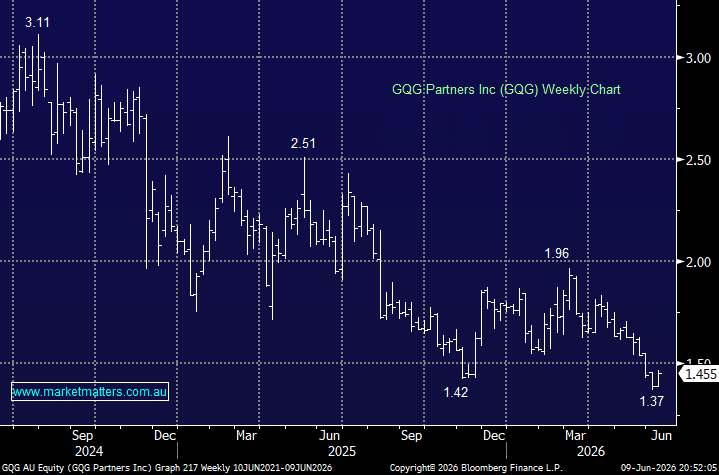

GQG Partners has been one of the more frustrating positions in our portfolios through 2026. The stock has fallen around 19% year-to-date, significantly underperforming the broader market, although investors have at least been compensated by a healthy income stream, with 7.19c per share already paid in dividends this year, equating to roughly 5%. Looking forward, the market is still forecasting a yield comfortably above 10% over the next twelve months.

The issue weighing on the stock is not difficult to identify. Investment performance has been weak relative to benchmarks, and in funds management, sustained underperformance almost inevitably raises concerns around client retention and future funds under management (FUM).

Recent monthly flow data highlights the challenge. While the pace of redemptions has moderated, the direction remains negative.

- January: -US$4.2bn

- February: -US$3.2bn

- March: -US$1.2bn

- April: -US$1.4bn

The trend is clearly improving; however, investors have yet to see the one thing that matters most – a return to positive net inflows. Until that occurs, concerns around earnings sustainability are likely to persist.

Performance has also been somewhat frustrating from a timing perspective. During the March quarter, when technology stocks stumbled and investors rotated toward more defensive sectors, GQG’s portfolios performed materially better. The firm’s long-standing preference for quality businesses with strong cash flows and relatively limited exposure to the mega-cap technology trade worked in its favour.

Unfortunately, that tailwind proved short-lived. Over recent months, the market has reverted to rewarding technology and AI-related exposures, areas where GQG remains significantly underweight. In April, some strategies underperformed benchmarks by around 9%, while one-year relative performance remains approximately 20% behind benchmark levels.

This is important because the funds management industry tends to be highly performance-driven. Investors, consultants and platforms often focus heavily on three-year performance periods when assessing managers. While GQG’s longer-term track record remains impressive, outperforming benchmarks since inception in 2014 and over ten years, the three-year performance numbers have become problematic, running around 4% per annum below their benchmark. That’s precisely the type of statistic that can influence consultant ratings, platform recommendations and ultimately client flows.

The upcoming May FUM update, which should be out this week, therefore takes on increased importance. While we suspect outflows will remain meaningful, investors will be looking closely for evidence that the pace of redemptions is continuing to moderate. Markets are generally willing to look through weak conditions if they can see signs of stabilisation.

To GQG’s credit, client retention has actually been more resilient than many would have expected given the extent of recent underperformance. Total FUM still sits at a substantial US$166.9bn, suggesting investors have retained confidence in the longer-term investment process despite a difficult period.

From a portfolio construction perspective, GQG remains an interesting proposition because it effectively represents the opposite side of one of the market’s most crowded trades. At a time when investors have become increasingly concentrated in AI beneficiaries and large-cap technology stocks, GQG provides exposure to a manager that is positioned quite differently. If the technology trade were to cool, history suggests GQG’s style could once again come back into favour.

That dynamic makes the position easier to justify within our Growth Portfolio, where we already own technology exposure elsewhere. Within the Income Portfolio, however, the investment case has been more challenging. Our primary rationale there was income generation rather than style diversification, and ongoing share price weakness has inevitably tested our patience.

The valuation is where the story becomes particularly interesting. GQG currently trades on roughly 7x earnings and offers a forecast yield well above 10%. Those metrics suggest the market is pricing in a meaningful deterioration in earnings and dividend sustainability. Ultimately, one of two outcomes is likely. Either earnings continue to fall, and dividends are cut, validating the market’s concerns, or earnings prove more resilient than currently expected, in which case the stock looks materially undervalued and should eventually attract a higher multiple.

For now, we remain in the camp that believes valuation alone is not enough. The stock is undoubtedly cheap, but cheap stocks can remain cheap while fundamentals continue to deteriorate. The next FUM update should provide an important insight into whether the worst of the outflow cycle is behind the company.

At current levels, GQG appears to be pricing in a lot of bad news. However, before becoming more constructive, we would like to see clearer evidence that both performance and client flows are stabilising. If that occurs, today’s valuation could ultimately prove very attractive. Until then, patience remains warranted.

MM is cautiously bullish GQG ~$1.50

Add To Hit List