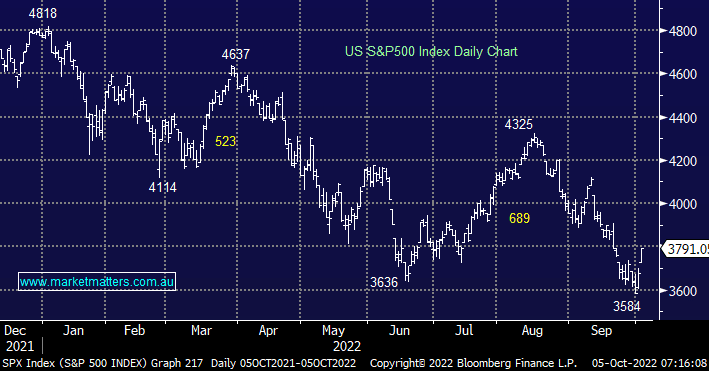

US indices rallied strongly overnight compounding Monday night’s gains pressuring shorts as indices enjoyed their best 2-day advance since 2020. Risk assets were helped by soft economic data which provided some optimism that the Fed won’t hike as aggressively as many feared e.g. the US job openings fell to a fresh 14-month low which should ease wage pressures. US 10-year yields slipped towards 3.6% after breaching 4% last week and the $US fell almost -1.4%.

The moves over the last 48 hours are significant but compared to the last 6 weeks they hardly register and we believe the complacent fund manager/trader positioning could be in for a very rocky road i.e. the “crowded trade” is underweight stocks & bonds while being long cash and the $US.

- We are bullish looking for a test of August highs into Christmas i.e. another ~13% upside.

MM remains bullish US stocks into Christmas

Add To Hit List