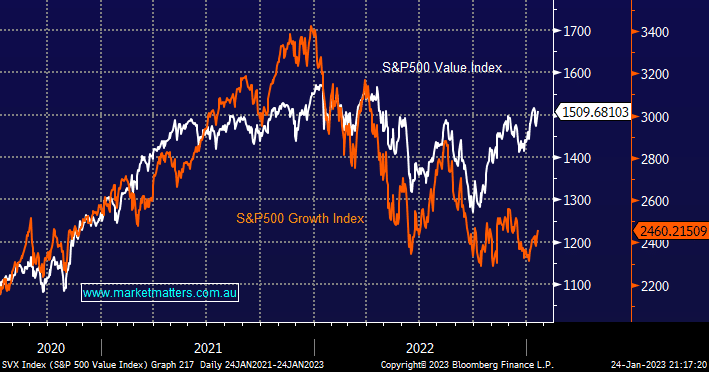

The US S&P500 Value Index is less than 5% below its all-time high while the Growth index continues to languish a painful 28% below its equivalent milestone. We may have seen the likes of Netflix (NFLX US) double in 6 months but they remain significantly below their late 2021 high. As subscribers know with interest rates soaring from their ultra-accommodative levels post Covid to arguably the new norm investors shouldn’t be surprised by the market rerating of the growth stocks.

- MM expects the Fed to push interest rates above 5% in early 2023 where they could easily remain for the rest of the year i.e. Jerome Powell et al will not want to appear too fickle after the steepest appreciation in rates the world has ever endured.

However recently MM has started to adopt a mild contrarian stance, at least over the short term, as we look for a recovery by tech names:

- we are targeting a short-term period of outperformance by the growth stocks assuming we are correct and the $US bounces after its 11% pullback from recent highs in Q4 of 0222.

- however, medium to longer term in line with our view that commodity prices trade a lot higher over the coming years the value stocks look set to outperform into 2024 and beyond.

Time will tell if this contrarian call proves on point but either way, our outlook over the coming years is the reason why MM has migrated to a mildly overweight stance towards the Resources Sector as opposed to underweight which we would have done had we not been bullish in the bigger picture i.e. we’re “tweaking around the edges” within our portfolios.

MM is bullish on the S&P500 Value Index medium to long term

Add To Hit List